CarInsurance.com Insights

- A new car can lose up to 10% of its value the moment you drive it off the lot.

- Gap insurance protects against owing more than your car is worth after a total loss.

- It’s optional coverage — not required by states — but often recommended for leased or financed vehicles.

When a new car loses value the moment you drive it off the lot, you could quickly owe more on your loan or lease than the car is worth. That’s where gap insurance comes in. This optional coverage bridges the gap between your vehicle’s actual cash value and your remaining balance if your car is totaled or stolen.

While it’s not required by law, gap insurance can save you thousands of dollars depending on how you financed your car and how quickly it depreciates.

What is gap insurance?

Gap insurance is designed to cover the gap between your vehicle’s actual cash value (ACV) and the amount you still owe on your lease or loan when your vehicle was totaled or stolen.

“In many circumstances, the consumer owes more money on the vehicle than it is worth,” says Nick Schrader with Texas General Insurance in Houston. “Gap coverage will pay the difference between the loan amount and the actual cash value. If the car is totaled in a catastrophic loss, the gap coverage will pay off the loan amount, even if the vehicle is depreciated to a lower amount.”

Suppose your insurer totals your vehicle due to damage by a covered peril. In that case, the insurer will pay you the actual cash value of your car, assuming you are carrying comprehensive and collision coverage. ACV is the actual value of the vehicle when it was destroyed. Your insurance company doesn’t consider how much you owe on the vehicle; the max they will pay out is the actual value of the car.

Do I need gap insurance?

Many car owners don’t understand how quickly a new car depreciates. While it varies by vehicle, in many cases, a new car can be worth 10% less than you paid as soon as you drive it off the lot.

Depreciation continues over the life of your car, especially in the first five years you own it. According to Carfax, the value of a new vehicle can drop by more than 20% after the first 12 months of ownership. Then, for the next four years, you can expect your car to lose roughly 10% of its value annually.

This means a new car can be worth as little as 40% of its original purchase price after five years, so an actual cash value insurance payout for your vehicle will likely be much less than what you owe for at least the first several years.

If you have a lease on a vehicle, your leasing company will typically require gap insurance; sometimes, it is part of the lease payment.

If you have purchased a new vehicle, gap insurance often makes sense, particularly if you struggle to cover the gap if your car was stolen or totaled. Here are a few situations where gap coverage makes sense:

- Made a small down payment on the vehicle.

- You have a long-loan term.

- You are out on the road a lot. The more you drive, the more likely an accident will happen.

- Your vehicle depreciates quickly; luxury cars and large SUVs tend to depreciate quickly.

- Your neighborhood is a hotbed for car theft. Gap coverage will step up if your vehicle is stolen.

Detailed guide on estimating your gap insurance cost with our calculator

Why buy gap insurance?

New cars tend to lose value once driven off the lot. While there isn’t an exact pre-determined rate at which vehicles depreciate, generally expect a new car to lose 20% of its value in the first year and roughly 15% per year until it’s about four years old.

Because newer vehicles depreciate so quickly, you may owe more on your car loan than the vehicle is worth if you total it in the first three years or so of ownership. This is where gap insurance steps up; it covers the difference between the ACV your insurer pays out and how much you owe on the vehicle loan.

If you are not carrying gap insurance, you will need to pay off the balance of your car loan out of pocket. Gap insurance typically must be purchased within 30 days of a new car purchase.

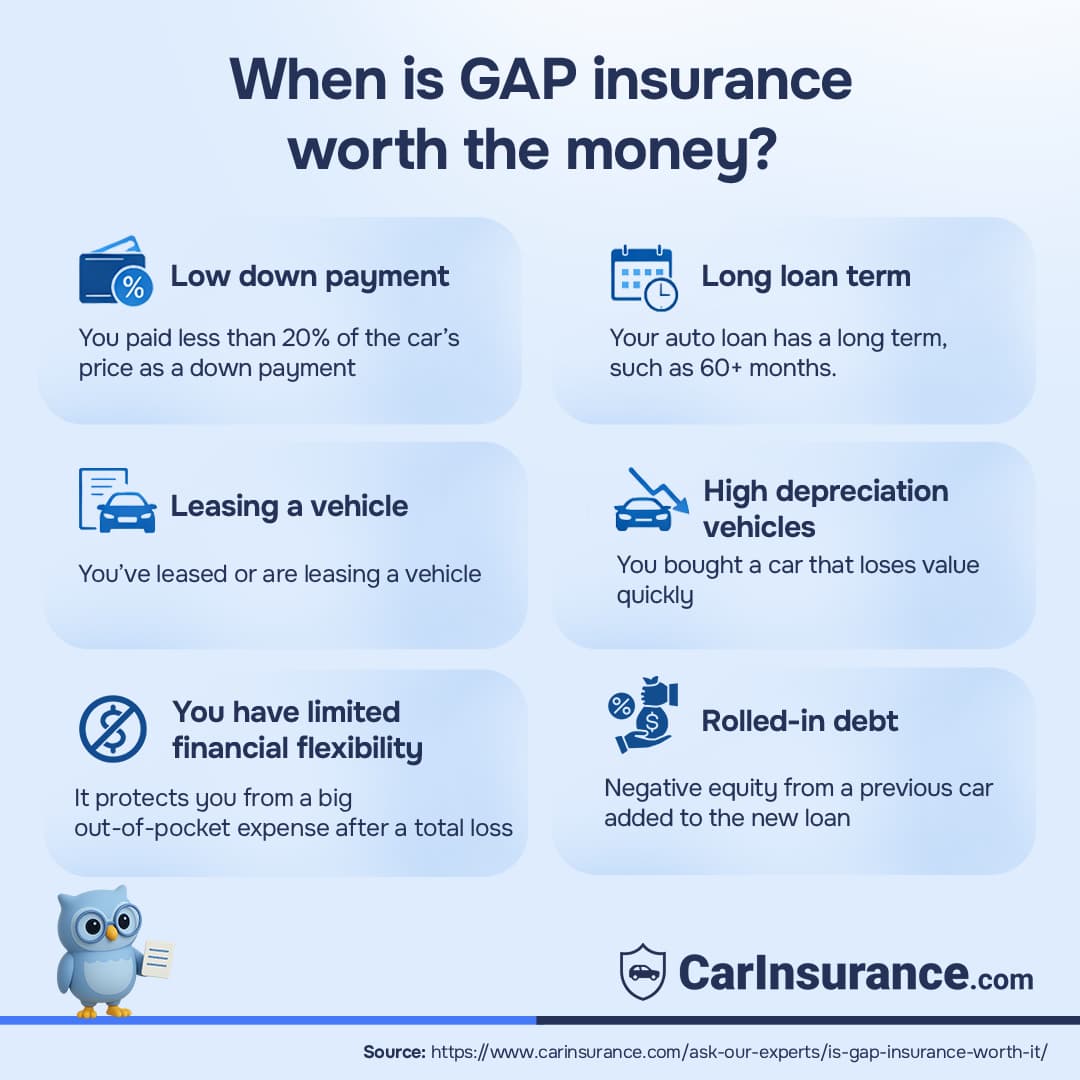

When gap insurance makes sense

You should strongly consider gap insurance if:

- You made a down payment of less than 20% on your car.

- Your loan term is longer than 60 months (5 years).

- You’re leasing your vehicle (many leasing companies require gap coverage).

- You bought a vehicle that depreciates quickly (SUVs and luxury cars often lose value faster).

- You rolled negative equity (money owed on a previous loan) into your new loan.

- You drive high annual mileage, which accelerates depreciation.

If several of these apply, gap insurance could save you thousands if your car is totaled or stolen.

When you might not need gap insurance

Gap insurance may not be necessary if:

- You made a large down payment (20% or more) on your car.

- Your loan balance is less than your car’s current market value.

- You’re driving an older, paid-off vehicle that has already depreciated significantly.

- You have short loan terms (36–48 months), so equity builds quickly.

- You could comfortably pay off the remaining loan balance out of pocket in case of a total loss.

In these cases, the extra cost of gap insurance may outweigh the benefits.

Speak with a friendly agent and get your quote in minutes!

What does gap insurance cover?

If your car is stolen or totaled, gap insurance will pay the difference between the vehicle’s ACV and the current balance on your loan or lease. In some cases, it will also cover your insurance deductible.

Policyholders often assume that if their car is stolen or totaled, their insurer will pay out the amount they paid for the vehicle or at least the amount they owe on their loan or lease.

Unfortunately, this is not the case. Your insurer will only pay out the ACV when it was stolen or totaled, leaving you to cover the loan balance. This is why most car insurance companies offer gap insurance as optional coverage.

You must also have comprehensive insurance and collision coverage to buy gap coverage, but your lender typically requires those if you lease or finance your car.

What isn’t covered by gap auto insurance?

Gap insurance will pay off your loan or lease amount after your insurer pays out the actual cash value of your stolen or totaled vehicle. However, gap insurance doesn’t cover several things, including overdue payments, security deposits and add-on equipment.

Here are some reasons gap insurance won’t pay due to some of the most common policy exclusions. Please note this list is not exhaustive; always read your policy fully to ensure you know all exclusions.

In most cases, gap insurance won’t pay for the following:

- Security deposits not refunded by the lessor

- Overdue lease/loan payments

- Costs for extended warranties, credit life insurance or other insurance purchased with the loan or lease

- Carry-over balances from previous loans or leases

- Financial penalties imposed under a lease for excessive use

- Amounts deducted by the primary insurer for wear and tear, prior damage, towing and storage

- Equipment added to the car by the buyer, meaning that only factory-installed equipment is covered

- Mechanical issues, such as engine or transmission failures, or any other car problems that are not losses covered by your car insurance policy

Does gap insurance cover theft?

Yes, gap insurance covers your car if it’s stolen and not recovered. It works with your comprehensive coverage for incidences of theft. Comprehensive will pay out up to the actual cash value of your car, minus your deductible if your car is stolen. Gap insurance would then pay the difference between the actual cash value payout and what you owe on your loan or lease.

How gap insurance works

Let’s look at an example of how gap coverage helps cover the gap between what you owe on your car loan or lease and the ACV insurance payout if your vehicle is stolen or totaled.

You buy a car that costs $25,000 and drive it off the lot. After paying the down payment, you owe $24,000 in car payments over five years (0% interest loan = $400 car payments). You purchase comprehensive and collision coverage with $500 deductibles.

You have an accident in the first year of ownership and your vehicle is totaled. The insurance company determines that the car’s actual cash value is only $22,000, but at the time of the loss, you still owe $23,500.

Gap insurance should pay the difference plus your deductible, totaling $2,000. It should be noted that not all gap policies pay the deductible.

Here is a quick breakdown:

- Loan payoff at the time of accident: $23,500

- Vehicle’s actual value at the time of accident: $22,000

- Your deductible: $500

- Collison coverage pays: $21,500 ($22,000 minus $500 deductible)

- Gap insurance payout covers the difference between what is owed and what your collision coverage pays, plus your deductible: $2,000

What is loan/lease coverage and how does it differ from gap coverage?

While the terms gap insurance and loan/lease coverage are often used interchangeably, they aren’t quite the same. Gap insurance will pay the difference between the amount you still owe on a vehicle and the actual cash value (ACV) paid out by your car insurance company, regardless of how much it is.

Lease/loan coverage, on the other hand, typically has limitations on how much it will pay out. In most cases, it limits coverage to 25% of the ACV of your vehicle. In most cases, lease or loan coverage doesn’t cover your deductible.

Example

ExampleIf you owed $25,000 on your car loan and the actual cash value of your vehicle was $20,000, then 25% of its value would be $5,000, which is the same as the gap of $25,000 due – $20,000 paid by the insurer. In this case, lease or loan insurance would have covered the whole amount, but that is not always true.

If I bought my car outright, do I need gap insurance?

There’s no reason to buy this coverage if you purchased the vehicle with cash or own it outright. Gap insurance only steps up when you owe more than the value of your vehicle. If you own the car outright, there would be no payout from gap coverage, so there is no need to carry this coverage.

If I paid a high down payment, do I need gap insurance?

Gap car insurance is only needed if you have negative equity in your car, meaning you owe more than the vehicle’s value. If you have paid a large down payment, 20% or more, gap insurance may not be necessary.

Depending on the vehicle and your loan amount, it can vary. In general, if you have made a down payment of at least 20%, you probably don’t need to carry gap coverage.

Is gap insurance required?

While you need gap insurance if you owe more on a vehicle than its value, gap coverage isn’t required by any state as part of your car insurance policy.

Gap insurance is optional; however, it’s not uncommon for lease contracts to include gap insurance. Sometimes, it’s called auto loan/lease coverage or loan/lease payoff coverage.

If your lessor requires gap insurance, they should include it within the lease’s cost. This means that the monthly price quoted by the dealer should consist of gap coverage if they require it.

While gap coverage is not legally required in any state, some financial institutions may want you to carry it as part of their loan requirements.

Is gap insurance worthwhile?

The answer to this question will usually depend on your situation. Gap insurance is often worth the cost of coverage in certain situations, while in others, you may be able to skip this coverage.

Gap insurance is usually very affordable. The average cost of gap insurance in the U.S. is $89 per year, which is about $7 per month. However, gap insurance premiums can vary depending on your age, insurance company and state.

Here are a few situations where gap coverage is probably a good idea:

- You owe more on your loan than what your car is worth

- You made a small down payment on your car, under 20%

- You don’t have enough savings to pay the gap if your car was totaled or stolen

- You drive more than 15,000 miles a year, as this accelerates your car’s depreciation

- Your vehicle type depreciates at a faster rate

If you have paid a 20% or higher down payment, have only financed the vehicle for a couple of years, don’t drive much or could easily cover the gap out of pocket, you may not need to carry gap insurance.

Does gap insurance always pay out?

Gap insurance only pays out if your vehicle is stolen or totaled, and you owe more on your car loan than the actual cash value payout from your collision or comprehensive.

If your collision or comprehensive claim is denied, your gap coverage will not pay out. There are also issues that could reduce your gap insurance payment. For instance, if you are late on a car payment before the claim, that amount will be deducted from your gap insurance payout.

When doesn’t gap insurance pay out?

When does gap insurance not pay? There are numerous circumstances when gap coverage won’t pay out. If your collision or comprehensive claim is denied, gap coverage will not pay out. The same is true if you didn’t pay your premium and your coverage lapsed.

Here are a few other situations where gap insurance will not offer coverage:

- Injuries: Gap insurance does not cover medical bills.

- Property damage you cause: Damage to a third party’s property isn’t covered by gap insurance.

- Damage that isn’t your fault and doesn’t result in a total loss: Even if your car sustains severe damage, gap insurance will only cover it if it is considered a total loss. If the other driver is at fault, their property damage liability should repair your car, or your collision insurance would cover it. In both cases, gap insurance would not cover the claim because the car wouldn’t be totaled.

Will gap insurance pay your deductible?

If you are wondering if gap insurance covers your deductible, the answer will vary depending on the specifics of your policy. Some policies pay the deductible, while others do not.

When it does pay the primary insurance deductible amount, the deductible amount isn’t reimbursed. Instead, the primary insurance deductible is taken from the payout of your totaled vehicle and covered as part of your unpaid loan balance, which gap insurance pays.

How do you get gap insurance for cars?

Gap insurance is a coverage that needs to be purchased shortly after buying or leasing a new car. You can usually purchase gap coverage from the following:

- The bank or financial institution holding your car loan

- The dealership where you bought the car

- Your car insurance company

- Purchase a policy from a company that specializes in stand-alone gap insurance policies

Can I get gap insurance without primary auto insurance?

No, you cannot purchase gap insurance unless you are carrying collision and comprehensive coverage. You will also need to be carrying the required minimum liability coverage mandated by your state.

Can I purchase gap insurance on a used vehicle?

Yes, it is often possible to purchase a gap policy on a used vehicle, but insurance companies’ guidelines vary. Many insurance companies will only write a gap policy on used vehicles that are less than three years old, some insurers lower that threshold to one year.

Once a car hits four or five years old, the benefits of a gap policy fade quickly, so it only makes sense to buy gap coverage for a used car that is 1 to 3 years old.

Is gap insurance acceptable as proof of insurance?

No, a gap insurance policy cannot be used as proof of insurance. A police officer, the Department of Motor Vehicles (DMV) or a loan officer will not accept a gap policy as proof of insurance. Gap insurance is not the right type of insurance needed to show financial responsibility for vehicle registration.

A police officer will want to see proof that you are carrying the state-required liability coverage, which would be in your primary car insurance policy. Your car insurance company will send an insurance card that you should keep in your vehicle as proof of insurance. It is usually possible to store an electronic version of your proof of insurance on your phone.

Can I get gap insurance on a loan that is not for a car?

No, you cannot get gap coverage for other loans. It doesn’t work with mortgage loans, credit lines, balloon payments or other types of non-vehicle-specific loans.

Can I buy gap insurance if my loan is from an individual?

No, insurers won’t offer coverage if your loan is through a private individual. When dealing with a bank or finance company, the insurer is aware of the terms, has access to the paperwork and works with a national company.

A private party loan makes it hard for the insurance company to be assured that the loan is only for the vehicle, payments are being made and the loan won’t be called in if you and the private party disagree.

Can you buy gap insurance anytime?

No, in most cases, gap insurance must be purchased within a short timeframe. While insurance companies’ terms will vary, gap insurance is generally available on new, used and refinanced vehicles that are less than a year old.

Some insurance companies will write gap coverage on vehicles up to 3 years old, but terms and guidelines vary so check with your insurer or agent regarding the availability of gap coverage.

Can you get gap insurance after an accident?

No. You cannot get gap insurance after an accident that results in your vehicle being totaled. If you are not carrying gap coverage, you will have to you will have to pay off your car loan out of pocket.

Gap insurance providers: Where to buy gap insurance?

Frequently Asked Questions: Gap insurance

Am I due a refund if I pay the car off? How do I get a refund?

Yes, getting a refund on your gap insurance is possible if you pay the car off, switch insurers or sell the car. It depends on how you pay for your coverage; it will impact whether you get a refund.

If you pay your car insurance premium yearly or every six months, you will be refunded for the months you have not used. If you pay monthly, you will only be refunded for the days you have not used in the most recent month.

Insurers will typically issue a refund when you cancel your coverage. Call your insurer, cancel your coverage and request a refund on the unused premium. Some insurers may require your cancelation notice in writing.

How can I cancel my gap insurance?

Canceling your gap coverage is just as easy as canceling any insurance coverage. Most insurers allow you to cancel your coverage by simply calling your insurance company or agent and letting them know the date of cancellation. Some insurance may require that you sign a cancellation form.

Check out our detailed guide on how to cancel your gap insurance

What is stand-alone gap insurance?

Gap insurance can be offered as an add-on to your standard car insurance policy or as a separate or stand-alone policy. This means it is a separate policy from your car insurance coverage.

It’s also possible to purchase a stand-alone gap insurance policy through your car dealer or lender when you buy or lease a vehicle. In most cases, purchasing gap coverage at the dealership or via your lender will be more expensive than getting it through your insurance company.

Another way to get gap coverage is to purchase a policy from a private third-party company offering gap insurance. These companies sell policies not tied to your loan or lease but will pay out if your vehicle is totaled.

Does a late car payment void a gap policy?

No, your car loan and gap insurance policy are separate items, so being late on your car payment doesn’t impact your coverage. However, any missed car payments will be deducted from your gap insurance payout.

Will gap insurance pay if the claim is denied?

No. If your claim is denied, your gap coverage will not pay out. Gap insurance only pays out for a vehicle that is totaled.

Is gap insurance transferable?

The answer will vary depending on your policy and where you purchased it. Each policy will be different so ask about transferability when purchasing the policy. In most cases an insurance company will allow you to transfer your gap coverage if you refinance your loan.

If you purchase gap insurance from your lender or leasing company the gap coverage is tied to your loan which makes it non-transferable. If you refinance a loan, the original loan is paid off, so the gap coverage no longer applies.

Does gap insurance come with a deductible?

No, gap insurance does not have a deductible to be paid when making a claim. There is a deductible with both collision and comprehensive coverage, which will have to be paid if your vehicle is totaled.

What is a gap insurance waiver?

A gap insurance wavier functions like gap insurance, but it is typically purchased from your lender/lease company or the dealership. A gap insurance waiver is typically paid for upfront or can be rolled into your car loan or lease payments.

If your vehicle is totaled or stolen, the gap insurance waiver will waive your obligation to pay off the remaining balance on the loan.

When did gap insurance start?

Gap coverage started in the early 1980s to help those insured who purchased a car and found themselves owning more than it was worth if it was in a total loss situation. The higher price of motor vehicles, longer-term auto loans and the increasing popularity of leasing in the 1980s led to the creation of gap protection.

How long does gap insurance last?

It will continue for the duration of your gap policy. You don’t need this coverage once you’ve paid off your car loan or even once you owe less than the actual cash value of your car. You should notify your insurer that you want to cancel the coverage at that time. Otherwise, it will remain in force until the end of the gap policy terms.

Get advice from an experienced insurance professional. Our experts will help you navigate your insurance questions with clarity and confidence.

Browse all FAQs