CarInsurance.com Insights

- Grace periods are not guaranteed — they vary by insurer and state.

- You may not have coverage during the grace period unless the insurer confirms it.

- Driving after expiration can lead to penalties, including fines or license suspension.

- A lapse in coverage can raise future premiums significantly.

- Immediate action can sometimes reinstate coverage without long-term impact.

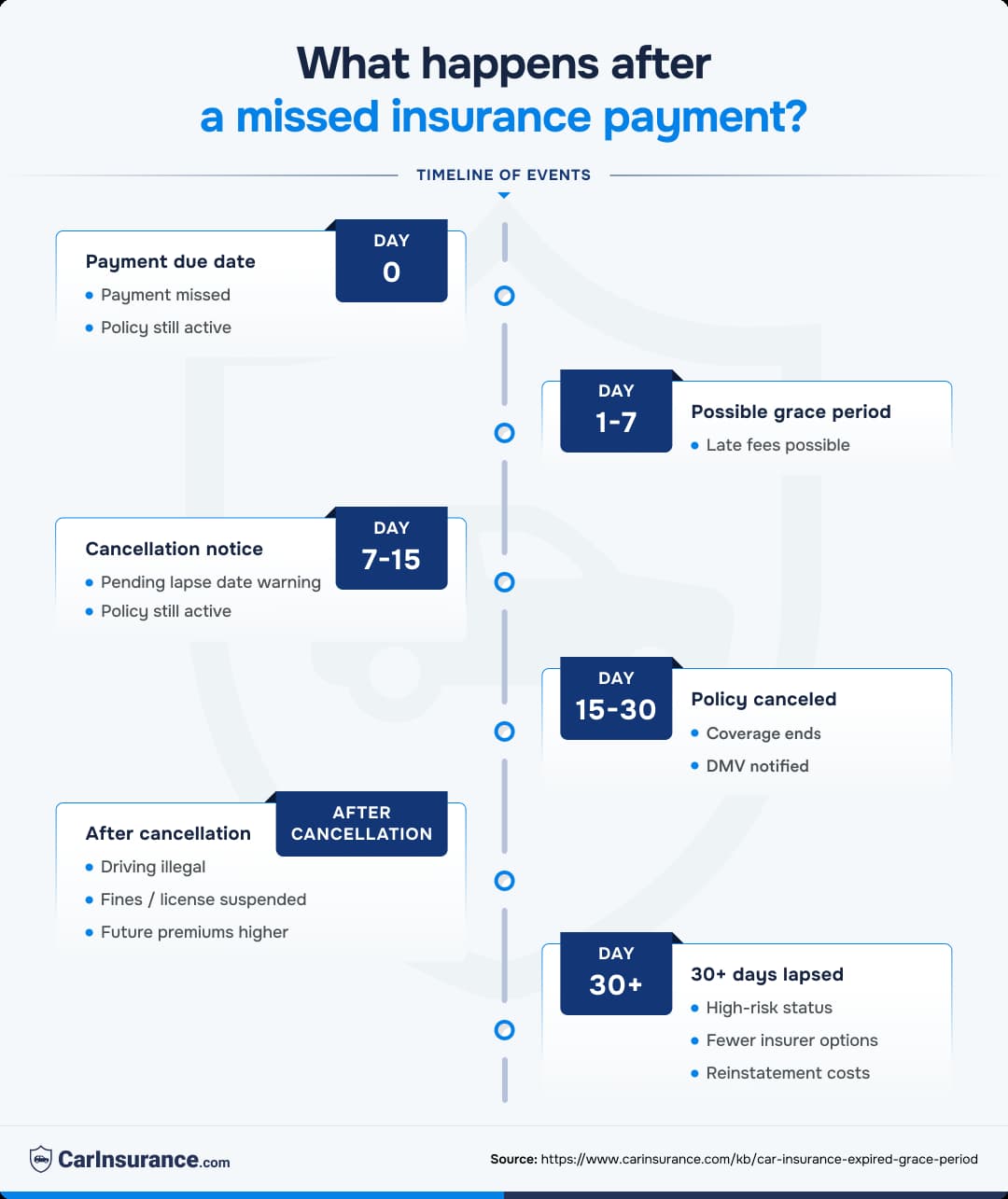

Is there a grace period for expired car insurance?

Some insurers offer a short grace period — typically 7 to 30 days — if you miss a payment or your policy expires. However:

- Grace periods are not required in every state.

- Terms differ by insurer.

- Coverage during the grace period may be suspended until payment is received.

What happens if your car insurance expires?

If your policy lapses:

1. You may have no legal coverage

Most states require continuous liability insurance. Driving uninsured can result in:

- Fines

- Registration suspension

- License suspension

- SR-22 filing requirements

2. You risk financial liability

If you cause an accident without coverage, you are personally responsible for:

- Property damage

- Medical bills

- Legal costs

3. Your future premiums may increase

Insurers view coverage lapses as higher risk. Even a short lapse can raise rates.

Sophie’s wise words

Sophie’s wise wordsNever assume you’re covered. Always confirm directly with your insurer. A grace period may exist, but it does not guarantee active coverage.

What is a coverage lapse?

A coverage lapse occurs when your policy ends and no replacement policy is active.

Common causes:

- Missed payments

- Non-renewal

- Policy cancellation

- Switching insurers without overlapping dates

Even one day without coverage can count as a lapse in many underwriting systems.

Speak with a friendly agent and get your quote in minutes!

Does insurance cover an accident during the grace period?

It depends.

Some insurers:

- Continue coverage during the grace period

- Reinstate coverage retroactively after payment

Others:

- Suspend coverage until payment is made

- Deny claims if payment wasn’t received before the accident

Always confirm:

- Whether coverage remains active

- Whether reinstatement is retroactive

Do not assume protection.

How to reinstate an expired car insurance policy

If your policy expired:

- Call your insurer immediately.

- Ask whether reinstatement is possible.

- Pay any overdue premiums.

- Request written confirmation of coverage status.

If reinstatement is not possible:

- Purchase a new policy immediately.

- Avoid driving until coverage is active.

- Expect potentially higher rates.

How long can you go without car insurance?

Legally, in most states: Zero days. Penalties escalate the longer the lapse continues.

If your insurer reports a lapse to the DMV, you may need to:

- Pay reinstatement fees

- Provide proof of insurance

- File SR-22 documentation (high-risk status)

How to avoid a car insurance lapse

Prevent future issues by:

- Enrolling in autopay

- Setting calendar reminders

- Confirming renewal dates annually

- Keeping updated contact and billing information

- Comparing quotes before renewal, but ensuring no coverage gap

When switching insurers, overlap policies by at least one day to avoid accidental lapses.

Is a short coverage lapse a big deal?

Even a short lapse can:

- Increase premiums

- Affect eligibility for preferred rates

- Trigger state penalties

- Require proof of financial responsibility filings

The financial impact often exceeds the cost of the missed premium.

Frequently Asked Questions: Car insurance grace period

How long is the grace period for car insurance?

It varies by insurer and state, typically between 7 and 30 days — but coverage may not remain active during that time.

Am I covered if I get into an accident during the grace period?

Not necessarily. Some insurers suspend coverage until payment is received. Always confirm directly.

Will a one-day lapse affect my rates?

It can. Many insurers factor any lapse into risk calculations.

Can I reinstate my policy after it expires?

Sometimes, if you act quickly. Call your insurer immediately to ask about reinstatement options.

What happens if I drive without insurance?

You may face fines, license suspension, vehicle impoundment, and higher future premiums.

Get advice from an experienced insurance professional. Our experts will help you navigate your insurance questions with clarity and confidence.

Browse all FAQs