CarInsurance.com Insights

- Non-owner SR-22 is liability-only car insurance for when you don’t own a car but need to file an SR-22 with your state to prove you meet coverage requirements.

- Non-owner SR-22 insurance costs $574 a year on average, with state rates ranging from $262 in South Dakota to $1,487 in New Jersey.

- There are three types of non-owner SR-22: SR-22 (most states), SR-22A (for low-level offenses in Georgia, Missouri, and Texas), and FR-44 (in Florida and Virginia, which have higher liability limits after a DUI).

- Most major insurers will file your SR-22 electronically with the DMV the same day you buy the policy, so you can start reinstatement without a wait.

- If your SR-22 lapses, your insurer will notify the state and your license will be suspended automatically.

- In many states, a lapse will restart the SR-22 requirements clock.

Non-owner SR-22 insurance is liability coverage for drivers who don’t own a car but need their insurer to file an SR-22 form with the state. It costs an average of $574 a year and proves you carry the minimum liability coverage your state requires, usually after a DUI, license suspension, or driving-uninsured conviction.

An SR-22 is not insurance. Rather, it’s a one-page certificate your insurer files with your state’s DMV to prove you have the required coverage. “Non-owner” means the insurance is designed for people without a registered vehicle, so it costs less than a standard owner policy.

This guide shows you who needs non-owner SR-22 insurance, what it covers, how much it costs in your state, and the five steps to get one.

What is non-owner SR-22 insurance?

Non-owner SR-22 insurance is a liability-only car insurance policy combined with a certificate of financial responsibility (SR-22). When your insurer files an SR-22 with your state, it proves that you carry the required minimum liability coverage. A non-owner SR-22 is designed for high-risk drivers who don’t own (or have regular access to) a vehicle but still need to comply with state car insurance laws after a DUI, license suspension, or a conviction for driving uninsured.

Sophie’s Tip

This is a state-required certificate, not a punishment. Most drivers who go through this are back to standard coverage in three years. However, these laws vary by state.

You can’t use a standard owner’s car insurance policy as a substitute. Owner policies are written for a specific vehicle; if you don’t own a car, that won’t work. A non-owner policy is written for you as a driver, providing bodily-injury and property-damage liability protection when you borrow or rent a car. The SR-22 certificate attaches to that policy and tells the DMV the coverage is real.

If you can’t show proof of insurance with an SR-22 on file, you could be charged with a misdemeanor in most jurisdictions, according to Mark Friedlander, senior director of media relations for the Insurance Information Institute. Consequences can range from license suspension to fines or jail time for repeat offenses.

Who needs non-owner SR-22 insurance?

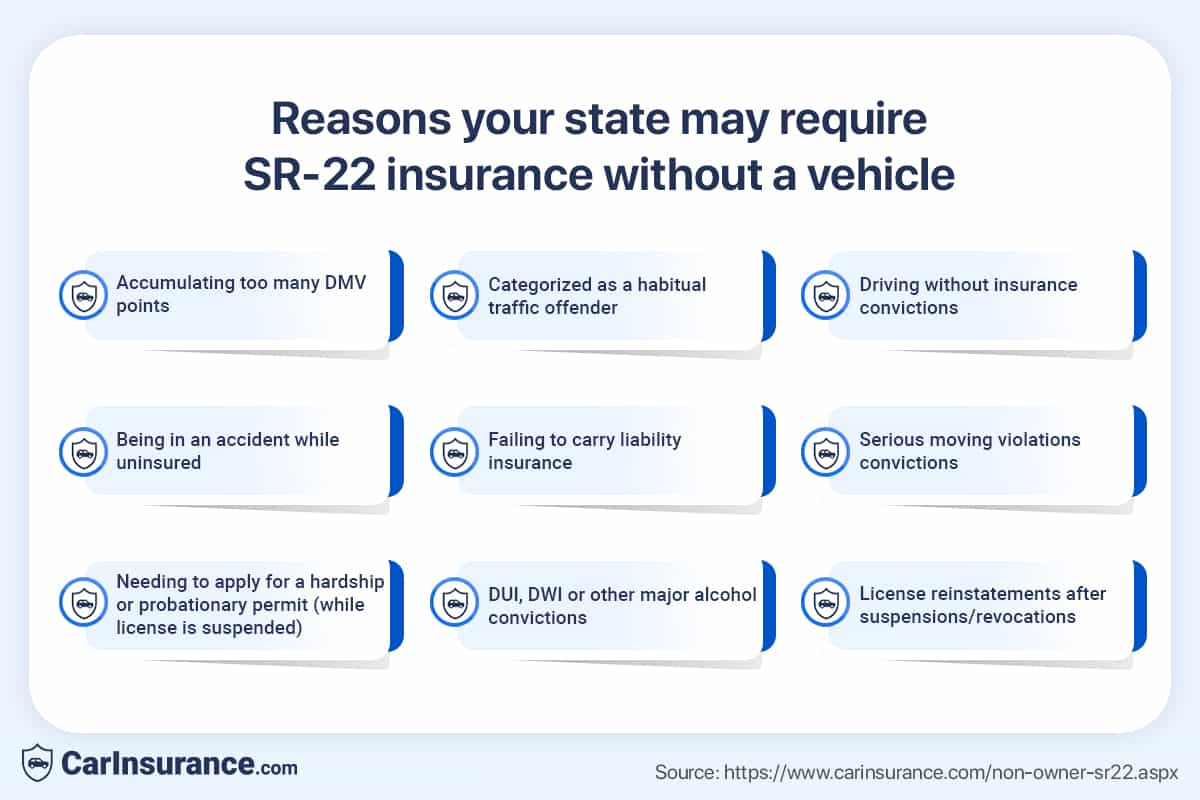

You’ll need non-owner SR-22 insurance if your state requires an SR-22 filing after a serious violation and you don’t own a car registered in your name. Common violations that trigger an SR-22 include a DUI conviction, a suspended license, or a court-ordered hardship permit.

A non-owner SR-22 is designed for one specific situation: you need to prove financial responsibility to the state but don’t have a car to insure.

High-risk drivers, or those with severe moving violations on their driving record, must often file an SR-22. If they rent or borrow a car rather than own one, they would need a non-owner SR-22.

According to Andrew Head, a Certified Financial Planner (CFP) and associate professor of finance at Western Kentucky University, the most common reasons your state could require non-owner SR-22 include:

- DUI, DWI, or other major alcohol-related convictions

- Your license has been suspended or revoked, and you’re trying to reinstate it

- Driving uninsured, or driving uninsured and causing an accident

- Accumulating too many points on your license or being labeled a habitual offender

- Reckless driving or other serious moving-violation convictions

- Applying for a hardship or probationary permit while your license is still suspended

- A court order tied to a specific civil or criminal case

In some states, the form you need may not be an SR-22, but rather an SR-22A (in Georgia, Missouri, and Texas) or an FR-44 (in Florida and Virginia). New York, Pennsylvania, Minnesota, and North Carolina don’t use SR-22s at all; instead, they rely on other ways to prove coverage.

SR-22 vs. SR-22A vs. FR-44: Which form does your state require?

Most states use the SR-22 form to confirm financial responsibility. Georgia, Missouri and Texas issue SR-22As for low-level offenses. Florida and Virginia require the more serious FR-44 after DUI convictions. All three forms can be satisfied with a non-owner liability policy when you don’t have a car.

If your state requires you to file proof of financial responsibility, the form you need depends on what you were convicted of and where you live. The table below shows details about each of the three forms and whether you could be eligible for a non-owner version.

| Form | Common triggers | States that use it | Liability minimum | Typical filing period | Non-owner eligible? |

|---|---|---|---|---|---|

| SR-22 | DUI, license suspension, driving uninsured, repeat moving violations | Most U.S. states (except NY, PA, MN, NC). FL and VA use FR-44 | State minimum liability — varies by state | 3 years (varies) | Yes — file with a non-owner liability policy |

| SR-22A | Lower-level financial-responsibility violations, such as failing to carry the minimum liability insurance | Georgia, Missouri, Texas | State minimum liability | Typically 2 years | Yes — file with a non-owner liability policy |

| FR-44 | DUI/DWI conviction | Florida, Virginia | higher than state min: 100/300/50 in FL, 60/120/40 in VA | 3 years | Yes, but the underlying non-owner policy must meet the higher FR-44 liability limits |

Confirm your specific form requirement and filing period with your state DMV before you buy a policy, since court orders can extend or shorten the standard period.

Speak with a friendly agent and get your quote in minutes!

How does non-owner SR-22 insurance work?

Non-owner SR-22 insurance works like this: You buy a non-owner liability policy from an insurer that handles SR-22 filings. Then, the insurer adds the SR-22 endorsement to your coverage and electronically files the form with your state DMV. At that point, the state recognizes the filing and either reinstates your license or maintains your driving privileges for the required period.

There is one wrinkle for people who don’t own a registered vehicle. Some insurers won’t write a non-owner policy at all, and others won’t pair one with an SR-22 filing. According to Friedlander, not owning a vehicle can make finding an insurance provider more difficult. The solution is to get the non-owner policy quoted first, then ask the insurer to attach the SR-22 endorsement before binding coverage.

See the section below on state filing rules to learn more about the states where an SR-22 form works differently.

What does non-owner SR-22 insurance cover?

Non-owner SR-22 insurance covers bodily injury and property damage liability when you drive a borrowed or rented car. It does not cover damage to the vehicle you’re driving. Typically, if you cause an accident, your non-owner policy pays only after the vehicle owner’s policy reaches its limit.

A non-owner SR-22 policy generally covers liability up to the limits you’ve purchased, and it’s secondary to the auto insurance policy of the vehicle’s owner. For example, if you borrow and drive a friend’s car, their policy will be primary, and yours secondary.

A non-owner SR-22 insurance policy will typically include the following:

Depending upon which state you live in and the car insurance company you’re using, you may also be able to buy other types of car insurance coverage, including:

What is not covered under a non-owner SR-22 insurance policy?

What is not covered under a non-owner SR-22 insurance policy? A non-owner SR-22 insurance policy is not a primary car insurance policy. It does not offer the physical damage coverages of collision or comprehensive policies. So, if you have an accident when driving a friend’s vehicle, any damages you incur won’t be covered by your non-owner policy.

How much does non-owner SR-22 insurance cost?

Non-owner SR-22 insurance costs $574 a year on average, with state rates ranging from $262 in South Dakota to $1,487 in New Jersey. Most drivers pay less than they would for an owner policy with state-minimum coverage, since a non-owner policy doesn’t cover physical damage to a vehicle.

Your cost will depend mostly on three things:

- Your state: Different states have different regulations and average claim costs vary widely.

- The violation that triggered the SR-22: A DUI, for example, roughly doubles the average.

- Your insurance company: The average rates with the most expensive insurance company are nearly 5 times higher than with the cheapest company.

It’s worth noting that a non-owner SR-22 is typically cheaper than an owner policy. According to 2026 Quadrant data, a non-owner SR-22 costs an average of $574 per year, compared to roughly $738 for a state-minimum owner policy. That’s about $164 a year less — the non-owner component keeps the price down even after adding the SR-22 filing.

There are two additional fees you should plan for. First, most insurers charge a one-time SR-22 filing fee, typically $15 to $50, which is paid alongside the policy. Second, some states also charge a separate license reinstatement fee. If that applies, it will be paid directly to the DMV.

Average annual non-owner SR-22 cost by state

South Dakota has the cheapest non-owner SR-22 insurance, with an average cost of $262 per year. New Jersey is the most expensive, with an average rate of $1,487, followed by Connecticut ($1,326) and Delaware ($1,076).

The average non-owner SR-22 rate varies so widely from one state to another because of differences in:

- How much liability coverage your state requires

- The average insurance payout per claim in your state

- How many uninsured drivers are on the roads in each state

Find out how your state ranks for a non-owner SR-22 policy in the table below.

| State | Average annual non-owner state-minimum rate | Avg annual non-owner SR-22 rate | % difference | $ difference |

|---|---|---|---|---|

| Alaska | $296 | $374 | 26% | $78 |

| Alabama | $469 | $604 | 29% | $135 |

| Arkansas | $440 | $679 | 54% | $239 |

| Arizona | $652 | $840 | 29% | $188 |

| California | $500 | $565 | 13% | $65 |

| Colorado | $506 | $689 | 36% | $183 |

| Connecticut | $1,054 | $1,326 | 26% | $272 |

| Washington, D.C. | $661 | $770 | 16% | $109 |

| Delaware | $936 | $1,076 | 15% | $140 |

| Florida | $668 | $818 | 22% | $150 |

| Georgia | $510 | $587 | 15% | $77 |

| Hawaii | $389 | $458 | 18% | $69 |

| Iowa | $280 | $328 | 17% | $48 |

| Idaho | $297 | $370 | 24% | $73 |

| Illinois | $518 | $740 | 43% | $222 |

| Indiana | $320 | $385 | 20% | $65 |

| Kansas | $408 | $507 | 24% | $99 |

| Kentucky | $499 | $552 | 11% | $53 |

| Louisiana | $410 | $473 | 15% | $63 |

| Massachusetts | $686 | $831 | 21% | $145 |

| Maryland | $516 | $686 | 33% | $170 |

| Maine | $271 | $304 | 12% | $33 |

| Michigan | $855 | $893 | 4% | $38 |

| Minnesota | $352 | $362 | 3% | $10 |

| Missouri | $346 | $359 | 4% | $13 |

| Mississippi | $474 | $525 | 11% | $51 |

| Montana | $412 | $489 | 19% | $77 |

| North Carolina | $681 | $729 | 7% | $48 |

| North Dakota | $353 | $408 | 16% | $55 |

| Nebraska | $402 | $508 | 26% | $106 |

| New Hampshire | $437 | $546 | 25% | $109 |

| New Jersey | $1,141 | $1,487 | 30% | $346 |

| New Mexico | $413 | $483 | 17% | $70 |

| Nevada | $823 | $984 | 20% | $161 |

| New York | $606 | $770 | 27% | $164 |

| Ohio | $291 | $365 | 25% | $74 |

| Oklahoma | $477 | $634 | 33% | $157 |

| Oregon | $644 | $796 | 24% | $152 |

| Pennsylvania | $279 | $347 | 24% | $68 |

| Rhode Island | $511 | $599 | 17% | $88 |

| South Carolina | $448 | $511 | 14% | $63 |

| South Dakota | $216 | $262 | 21% | $46 |

| Tennessee | $507 | $647 | 28% | $140 |

| Texas | $564 | $610 | 8% | $46 |

| Utah | $658 | $824 | 25% | $166 |

| Virginia | $549 | $741 | 35% | $192 |

| Vermont | $460 | $561 | 22% | $101 |

| Washington | $516 | $600 | 16% | $84 |

| Wisconsin | $398 | $466 | 17% | $68 |

| West Virginia | $442 | $496 | 12% | $54 |

| Wyoming | $270 | $307 | 14% | $37 |

If your state’s average rates are high, it could be worth getting a quote from a regional company. Regional insurance companies often beat national-carrier rates by hundreds of dollars.

How much does non-owner SR-22 insurance cost with a DUI, by state?

Non-owner SR-22 insurance when you have a DUI costs an average of $1,040 a year. The steepest markups are in:

- North Carolina (339% higher than the non-owner base rate)

- Hawaii (254% higher)

- Pennsylvania (173% higher)

- California (165% higher).

The smallest markups are in Texas (27%), New York (30%), and New Jersey (36%).

A DUI conviction is more likely to affect your rate than any other single factor. Insurers will categorize you as a high-risk driver, which will increase your rate. The size of the increase depends on your state regulations. Some states cap how much insurers can raise rates after a single violation; others don’t.

The table below shows the state minimum rate for a non-owner with one DUI in each state.

| State | Average non-owner annual rate | Average annual non-owner SR-22 with 1 DUI | % difference | $ difference |

|---|---|---|---|---|

| Alaska | $296 | $497 | 68% | $201 |

| Alabama | $469 | $788 | 68% | $319 |

| Arkansas | $440 | $772 | 75% | $332 |

| Arizona | $652 | $1,439 | 121% | $787 |

| California | $500 | $1,323 | 165% | $823 |

| Colorado | $506 | $1,182 | 134% | $676 |

| Connecticut | $1,054 | $2,422 | 130% | $1,368 |

| Washington, D.C. | $661 | $978 | 48% | $317 |

| Delaware | $936 | $1,739 | 86% | $803 |

| Florida | $668 | $1,348 | 102% | $680 |

| Georgia | $510 | $821 | 61% | $311 |

| Hawaii | $389 | $1,375 | 254% | $986 |

| Iowa | $280 | $414 | 48% | $134 |

| Idaho | $297 | $517 | 74% | $220 |

| Illinois | $518 | $917 | 77% | $399 |

| Indiana | $320 | $547 | 71% | $227 |

| Kansas | $408 | $739 | 81% | $331 |

| Kentucky | $499 | $1,156 | 132% | $657 |

| Louisiana | $410 | $779 | 90% | $369 |

| Massachusetts | $686 | $1,382 | 102% | $696 |

| Maryland | $516 | $969 | 88% | $453 |

| Maine | $271 | $462 | 70% | $191 |

| Michigan | $855 | $2,009 | 135% | $1,154 |

| Minnesota | $352 | $560 | 59% | $208 |

| Missouri | $346 | $498 | 44% | $152 |

| Mississippi | $474 | $959 | 102% | $485 |

| Montana | $412 | $741 | 80% | $329 |

| North Carolina | $681 | $2,988 | 339% | $2,307 |

| North Dakota | $353 | $532 | 51% | $179 |

| Nebraska | $402 | $987 | 145% | $585 |

| New Hampshire | $437 | $779 | 78% | $342 |

| New Jersey | $1,141 | $1,547 | 36% | $406 |

| New Mexico | $413 | $811 | 96% | $398 |

| Nevada | $823 | $1,530 | 86% | $707 |

| New York | $606 | $790 | 30% | $184 |

| Ohio | $291 | $641 | 120% | $350 |

| Oklahoma | $477 | $1,031 | 116% | $554 |

| Oregon | $644 | $1,242 | 93% | $598 |

| Pennsylvania | $279 | $761 | 173% | $482 |

| Rhode Island | $511 | $935 | 83% | $424 |

| South Carolina | $448 | $650 | 45% | $202 |

| South Dakota | $216 | $376 | 74% | $160 |

| Tennessee | $507 | $1,160 | 129% | $653 |

| Texas | $564 | $717 | 27% | $153 |

| Utah | $658 | $1,057 | 61% | $399 |

| Virginia | $549 | $1,358 | 147% | $809 |

| Vermont | $460 | $899 | 96% | $439 |

| Washington | $516 | $936 | 81% | $420 |

| Wisconsin | $398 | $683 | 71% | $285 |

| West Virginia | $442 | $633 | 43% | $191 |

| Wyoming | $270 | $577 | 114% | $307 |

If you’re shopping for insurance after a DUI, see below for practical steps to lower your non-owner SR-22 costs.

Non-owner SR-22 insurance costs by company

GEICO offers the cheapest average annual rate among the eight top nationwide insurance companies at $481, followed by Travelers at $520. (Technically, USAA is the cheapest at $232 a year, but it’s only available for military families.) Among regional carriers, Auto-Owners offers the cheapest non-owner SR-22 insurance at $207 annually, on average, and it’s available in 20 states.

Rates from national carriers

The table below shows the average annual and monthly costs for non-owner SR-22 coverage with national insurance companies.

| Company | Average annual cost | Average monthly cost |

|---|---|---|

| GEICO | $481 | $40 |

| Travelers | $520 | $43 |

| State Farm | $762 | $64 |

| Nationwide | $780 | $65 |

| Progressive | $782 | $65 |

| Farmers | $822 | $69 |

| Allstate | $910 | $76 |

| USAA* | $232 | $19 |

*USAA is only available to military community members and their families.

Rates from regional carriers

The table below shows the average annual and monthly costs for non-owner SR-22 coverage with regional insurance companies.

| Company | Average annual cost | Average monthly cost | States available |

|---|---|---|---|

| Auto-Owners | $207 | $17 | 20 |

| Safety Insurance | $303 | $25 | 2 |

| Kemper | $328 | $27 | 1 |

| Vermont Mutual | $347 | $29 | 1 |

| Westfield Insurance | $375 | $31 | 2 |

| Erie Insurance | $446 | $37 | 8 |

| American Family | $622 | $52 | 2 |

| Iowa Farm Bureau | $631 | $53 | 6 |

| North Carolina Farm Bureau | $680 | $57 | 1 |

| Mercury Insurance | $767 | $64 | 4 |

| American National | $989 | $82 | 2 |

Sophie’s Tip

Get quotes from at least three carriers, and include one regional if any operate in your state. Regional carriers often beat national-carrier averages by hundreds of dollars on the same driver profile.

How to get non-owner SR-22 insurance

To get non-owner SR-22 insurance, you’ll need to confirm which form your state requires, find a company that files SR-22s for non-owners, and buy a non-owner liability policy. Then, the insurer will file the SR-22 electronically with your state’s DMV. You’ll need to maintain continuous coverage for the required filing period.

Follow the steps below to buy non-owner SR-22 insurance.

- Find an insurance company that files SR-22s for non-owners. Not every insurer writes non-owner policies, and not every non-owner writer will attach an SR-22, so you’ll need to shop around. National companies that consistently handle both include GEICO, Travelers, State Farm, Nationwide, Progressive, and Allstate. Among regional insurance companies, check with Auto-Owners, Erie, Kemper and Westfield, all of which typically handle non-owner SR-22s in the states they serve.

- Buy a non-owner liability policy. Quote the policy without the SR-22 endorsement first. Then ask for the SR-22 to be attached before you pay and finalize your coverage. Confirm that the insurance company will file the form electronically with the DMV rather than requiring you to file a paper form yourself.

- The insurer files the SR-22 electronically with the DMV. This typically happens the same day you pay for the policy. The state acknowledges the filing within 24-72 hours, depending on the DMV.

- Maintain continuous coverage for the required filing period. This is critical if you want to keep your license. Don’t let the policy lapse, even for a moment. The insurer is required to notify the state if your policy is canceled, which triggers automatic license suspension in most states.

State filing rules: Where SR-22 works differently

Most states use the SR-22 form, but the rules can vary. Florida and Virginia use the FR-44 form instead and require higher liability minimums. New York, Pennsylvania, Minnesota, and North Carolina don’t use an SR-22 and instead rely on equivalent proof-of-coverage forms filed with the state. Georgia, Missouri and Texas use SR-22A for some lower-level offenses.

| State | Details |

|---|---|

| California | Uses SR-22. Typical filing period: 3 years. Online filing supported. Common after a DUI conviction or driving uninsured. See California non-owner SR-22 page for state-specific rates. |

| Texas | Uses SR-22 and SR-22A (the latter for some financial-responsibility-only offenses). Typical filing period: 2 years. Online filing supported by most major carriers. |

| Florida | Uses FR-44, not SR-22. Requires higher liability limits: 100/300/50 (vs. state-min 10/20/10). Typical filing period: 3 years from license reinstatement, not conviction date. |

| North Carolina | Uses DL-123 financial-responsibility filing. DUI markups are the highest in the country (339% over the non-owner base). Typical filing period: 3 years. |

| Tennessee | Uses SR-22. Typical filing period: 3 to 5 years, depending on offense. Online filing supported. |

| South Carolina | Uses SR-22. Typical filing period: 3 years. Online filing supported. |

| Ohio | Uses SR-22. Typical filing period: 3 to 5 years. Online filing supported by most major carriers. |

| Illinois | Uses SR-22. Typical filing period: 3 years. Online filing supported. |

| Georgia | Uses SR-22 standard, SR-22A for low-level financial-responsibility violations. Filing period varies (typically 2–3 years). |

| Virginia | Uses FR-44 after DUI, SR-22 for some other offenses. FR-44 requires 60/120/40 liability limits. Typical filing period: 3 years from license reinstatement. |

| New York | Doesn’t use SR-22. The DMV monitors proof of insurance directly through the FS-1 insurance ID card system. Drivers transferring from SR-22 states may not need to file new paperwork. |

| Pennsylvania | Doesn’t use SR-22. The PennDOT uses an internal financial-responsibility filing handled directly by insurers. |

Confirm your state’s specific rules with the DMV before buying coverage, as court orders can override standard requirements.

How to reinstate your license after an SR-22 lapse

If your non-owner SR-22 lapses, your insurer will notify the state, and your license will typically be suspended automatically within days. To reinstate your license, you’ll need to restore the required car insurance coverage, pay state reinstatement fees and file (or have your insurer file) a new SR-22. If your state imposes an extended filing period, you’ll need to serve that, too. Many states restart the SR-22 clock from day one if your coverage lapses.

Sophie’s Tip

A lapse usually means the SR-22 clock restarts, not that you’ve lost your case. The faster you restore coverage, the less damage there is.

Here is a 6-step recovery checklist to follow to reinstate your license after a lapse in SR-22 coverage:

Step 1. Restore your non-owner liability policy immediately. If you can manage to reinstate coverage the same day, it keeps the lapse window short and could help you avoid the need to maintain SR-22 insurance longer. Some insurers offer a grace period and will reinstate the original policy if you pay the missed premium within a few days.

Step 2. Confirm the new SR-22 has been filed. Even if you reinstate your policy with the same insurer, the SR-22 endorsement typically has to be re-filed. Ask your insurer for written confirmation that the new SR-22 was transmitted to the state DMV.

Step 3. Pay your state’s license reinstatement fee. This is a separate fee paid directly to the DMV, not your insurer. Amounts vary by state, but they’re typically between $50 and $300.

Step 4. Confirm your reinstatement status with the state. Some DMVs take one to two weeks to update your record to reflect the reinstatement and you could cause even more problems for yourself if you drive without it. Get a printed or digital confirmation before driving.

Step 5. Resume continuous coverage. The replacement SR-22 begins an all-new monitoring period, effectively restarting the clock. If you let your insurance lapse again, it could extend the filing period even further or trigger a longer suspension.

Step 6. Set up payment safeguards. Reduce the risk of accidentally letting your coverage lapse with auto-pay, multiple billing reminders and by confirming your insurer’s lapse-notification process. Find out if your insurer offers a grace period before you actually need it.

How to lower your non-owner SR-22 insurance costs

There are five ways you could lower the cost of non-owner SR-22 insurance: get quotes from at least three carriers, check if your state issues an SR-22A form for your offense, avoid a coverage lapse during the filing period, bundle your policy with renters insurance and maintain a clean driving record.

Follow the tips below to save money on non-owner SR-22 car insurance:

- Get quotes from at least three insurers — including one regional insurer. Friedlander recommends mixing national and regional carriers when shopping with an SR-22. Regional companies such as Auto-Owners ($207) often cost less than half the average rate for a national insurer ($481 at GEICO).

- Check if your state issues SR-22A. Georgia, Missouri and Texas use the lighter (and often cheaper) SR-22A form for some lower-level financial-responsibility offenses. However, this doesn’t apply to DUIs. Ask your DMV if SR-22A applies to your situation, as it could have a smaller impact on your rates than an SR-22.

- Avoid any coverage lapse. Even a one-day lapse triggers a notification to the DMV, resulting in a license suspension and, in most states, a restart of your filing clock. That could prove more expensive than simply paying your premium.

- Bundle policies for a discount. Friedlander notes that common discount sources for SR-22 drivers include bundling auto policies with renters or other insurance, paying in full, signing up for electronic communications and signing up for usage-based telematics programs. Each one can trim a little off your base rate.

- Maintain a clean record during the filing period. Each new violation you get during the SR-22 filing period can extend the SR-22 requirement and add to your rate surcharge. Insurance companies reprice annually and a year with a clean record can usually drop your rate meaningfully when it’s time to renew.

Compare non-owner SR-22 quotes from multiple carriers using our car insurance comparison tool. Your information stays private until you choose to share it with a carrier.

People also ask

Can I get an SR-22 without owning a car?

Yes. A non-owner SR-22 policy is designed specifically for this situation: Drivers who need to file an SR-22 but don’t own a car registered to their name. You buy a non-owner liability policy and the insurer files the SR-22 certificate electronically with your state’s DMV. Not all insurers will handle SR-22 forms. Coverage applies when you borrow or rent a car. The SR-22 certificate proves to the state that you carry the minimum liability coverage required by your license.

Do I need an SR-22 in California if I don’t own a car?

Yes, if a California court or the DMV has required it after a violation such as a DUI, license suspension, or driving uninsured. California uses the standard SR-22 form. The typical filing period is three years and online filing is supported by most major insurance companies. Check the California non-owner car insurance page for state-specific rates.

What happens if my non-owner SR-22 lapses?

If your insurance lapses, your insurer notifies the state and your license is typically suspended automatically. To reinstate it, you must restore the policy, file a new SR-22, pay any state reinstatement fees, and, in most states, serve a new filing period. See How to reinstate your license after an SR-22 lapse above for the full six-step recovery walkthrough.

How do I cancel my non-owner SR-22 if I buy a car?

Rick Estrella, director of operations for Estrella Insurance, says you should replace the non-owner policy with a regular owner policy that includes the SR-22 certificate. Your insurer can usually transfer the SR-22 filing to the new policy without a coverage gap. It’s very important that you don’t simply cancel the non-owner policy. Wait until the new owner’s policy with SR-22 is active, as a gap in coverage can trigger a state suspension.

Key takeaways: Non-owner SR-22 insurance

- SR-22 is not insurance. It’s a state-issued certificate proving you carry the minimum auto liability coverage required by your state.

- The cost of non-owner SR-22 insurance averages $574 a year, with state rates ranging from $262 (South Dakota) to $1,487 (New Jersey).

- The cost of non-owner SR-22 insurance with a DUI averages $1,040 a year. North Carolina has the steepest markup at 339% over the non-owner base.

- The cheapest national insurance company open to everyone is GEICO, with an average annual rate of $481. Among regional carriers, Auto-Owners leads at $207 and is available in 20 states.

- SR-22 filing fees are typically $15 to $50 and paid alongside your premium. Most insurers file your form electronically the same day you buy.

- The required filing period is usually three years, but can be up to five years in some states. A lapse in coverage triggers automatic license suspension and often restarts your filing clock.

Frequently Asked Questions

Does non-owner SR-22 insurance cover any car I drive?

It covers liability when you drive a borrowed or rented car you don’t regularly use. It does not cover damage to the car you’re driving and it does not cover a vehicle titled in your name. If you drive the same person’s car more than occasionally, the insurer may decline a claim, since you’d need owner coverage at that point.

Can I move to a different state with a non-owner SR-22?

Yes, but the rules change at the state line. Notify your current insurer about the move. Verify whether your new state still requires SR-22, requires FR-44 instead (Florida or Virginia), or doesn’t require SR-22 at all (New York, Pennsylvania, Minnesota and North Carolina). Maintain continuous coverage throughout the move to avoid restarting your filing clock.

How long do I need to carry non-owner SR-22 insurance?

Most states require non-owner SR-22 filings for 3 years, but some extend the requirement to 5 years for certain offenses. Florida and Virginia require FR-44 for three years from the date of license reinstatement, not from the conviction date. Confirm your specific filing period with your state DMV.

Can I get non-owner SR-22 insurance with a suspended license?

Yes. In most states, buying a non-owner policy and filing an SR-22 are the first steps toward reinstating your suspended license. Once the state acknowledges the filing — usually within 24 to 72 hours — you can apply for reinstatement and resume driving once the DMV restores your license.

Can I switch from a non-owner SR-22 to a regular policy later?

Yes. When you buy or lease a car, you replace the non-owner policy with a standard owner policy that includes an SR-22. Your insurer can usually transfer the SR-22 filing to your new policy, avoiding a gap in coverage. Don’t cancel the non-owner policy until the owner policy with SR-22 is active, or your license could be suspended.

What’s the difference between an SR-22 and non-owner insurance?

An SR-22 is a state-filed certificate proving you carry the legally required minimum liability coverage. Non-owner insurance is a liability car insurance policy, the certificate of which is attached to. You can have non-owner insurance without an SR-22, but you cannot have an SR-22 without an insurance policy.

Can I buy non-owner SR-22 insurance online?

Yes, in most states. Major carriers, including Progressive, GEICO, State Farm, Travelers and Nationwide, will quote and activate non-owner SR-22 policies online. The insurer files the SR-22 electronically with your state DMV the same day you pay. A few states still require the insurer to mail a physical filing, so check with your state’s requirements.

What happens if I don’t keep my non-owner SR-22 insurance active?

Your insurer notifies the state of the cancellation, which triggers automatic license suspension in most states. You’ll typically face reinstatement fees, a restarted SR-22 filing period in many states, and higher renewal premiums afterward, since insurance companies reprice you to include a record of lapsed coverage.

Resources & Methodology

Methodology

CarInsurance.com analyzed non-owner state-minimum liability rates with SR-22 filing across states, collected from Quadrant Information Services.

The rates are based on sample profiles of 40-year-old male and female drivers with 10,000 miles per year and a 12-mile daily commute.

DUI rates use the same driver profiles with one DUI conviction on record. All rates are annual averages and are intended for comparison purposes. Your actual rate will vary based on your driving history, the insurer you choose, your state’s minimum requirements and other underwriting factors. Read the detailed methodology for more information.

Get advice from an experienced insurance professional. Our experts will help you navigate your insurance questions with clarity and confidence.

Browse all FAQs