CarInsurance.com Insights

- Since insurers place binding restrictions on policy changes once a storm is named, add comprehensive coverage to your policy before hurricane season begins on June 1.

- Comprehensive coverage is imperative in protecting your vehicle against storm damage.

- Hail generates the most car insurance claims by volume – 12% of comprehensive claims in the U.S.

- Flooding generates the most expensive insurance claims, often because water-damaged electronics result in the vehicle’s total loss.

- The January 2025 Southern California wildfires cost $41 billion in economic losses.

To ensure you know what to do when weather strikes, explore some of the most common weather-related car insurance claims and what steps to take during the aftermath.

Keep in mind that once a storm has been named, you won’t be able to add or change your insurance coverage. You must have your coverage in place beforehand.

| Term | Plain-language definition |

|---|---|

| Comprehensive coverage | The auto policy component that pays for non-collision damage, including weather events — hail, floods, wildfires, falling trees and more. Optional in most states, but essential for weather protection. |

| Actual cash value (ACV) | Your vehicle’s market value at the time of loss, after depreciation. Not what you paid or what it would cost to replace — typically lower than both. |

| Total loss | Declared when repair costs exceed the insurer’s threshold — typically 70–80% of ACV, varying by state and insurer. |

| Binding restriction | A temporary freeze on new coverage additions when a named storm or severe weather watch is issued. Coverage must be in place before the restriction activates. |

| Deductible | The amount you pay out of pocket before insurance covers the remainder. Common range: $250-$1,000. Higher deductible = lower premium, but more out-of-pocket after a claim. |

Which weather events cause the most car insurance claims?

Severe thunderstorms and hail cause the most car insurance claims. Hail causes the most car insurance claims by volume. Nearly 12% of all comprehensive claims filed in 2023 were for hail, up from 6.8% in 2022, according to the Texas Coalition for Affordable Insurance Solutions.

“The assessed annual risk from frequency perils, particularly losses from severe thunderstorms, winter storms, wildfires, and inland floods, accounts for a 12% greater share of the total modeled risk in 2025 over 2024,” risk-modeling company Verisk said in its report “Modeling Insured Catastrophe Losses: A Global Perspective for 2025.”

Furthermore, the report states that, specifically for severe thunderstorms, there’s a 59% increase in events generating insured losses exceeding $1 billion from 2020 to 2024, compared with the prior five years.

Wildfire poses an ongoing risk to the American West: “ The Verisk Wildfire model for the United States, for example, shows a markedly increased hazard relative to historical records in most, but not all, locations. This signal reflects how well-understood, large-scale warming and drying connect to the mechanisms underlying wildfire,” according to Verisk.

Hurricanes and tropical storms along the Gulf and Atlantic coasts cause claims clusters that can clutter appraisers’ desks in those regions for months at a time.

What does car insurance actually cover when weather damages your car?

If your car is damaged during a storm or other weather event, comprehensive coverage pays to repair or replace it, not collision or liability coverage. Comprehensive car insurance typically covers:

- Hail dents

- Flood damage

- Hurricane debris

- Tornadoes

- Wildfires

- Falling trees

- Ice damage

If you don’t carry comprehensive coverage (for example, if you have state minimum coverage), any repair costs come out of your pocket. The table below shows common weather events and the insurance coverage that applies.

If you don’t have comprehensive coverage, you may be able to get federal disaster assistance to help pay for damage and weather-related costs, according to the Federal Emergency Management Agency.

Sophie’s Tip

If you live in a state with an active hurricane corridor — Florida, Louisiana, Texas, the Carolinas — the best time to add comprehensive coverage is before June 1, not after you hear the first storm named. Once a watch is issued, most insurers freeze coverage changes.

Which states have high weather-related auto claims?

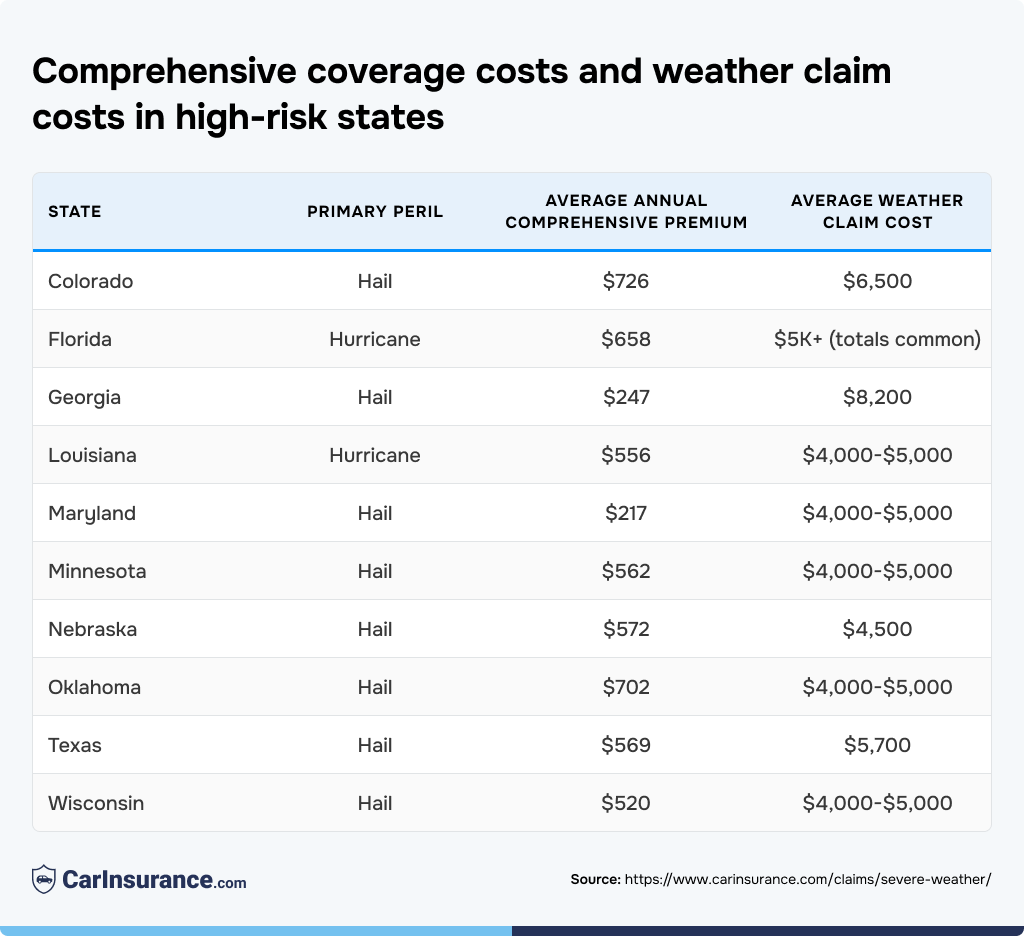

Texas recorded the most hail events of any state in 2023, with more than 1,100 recorded, according to the Texas Department of Insurance. Florida drivers filed more than 80,000 auto claims for damage caused by Hurricanes Helene and Milton, according to a ProgramBusiness report. And in Georgia, Hurricane Helene flooding damaged 16,800 vehicles, according to CARFAX. Where you park your car is one of the most significant factors in your comprehensive coverage cost.

According to NOAA data, Michigan saw more than 100 hail events in both 2023 and 2024, following seven straight years below that threshold.

The California Department of Insurance notes that wildfires generated at least 5,597 claims as of Feb 5, 2025, though the number of destroyed vehicles is higher. Similarly, while Florida hurricane-related auto insurance claims topped 88,000, CARFAX estimates 138,000 total vehicles were damaged.

Overall, the first half of 2025 was the most expensive on record for weather-related damage. Fourteen events caused an estimated $101.4 billion in damage, according to Climate Central, which has tracked climate disasters since 1980.

According to Gallagher Re’s “Natural Catastrophe and Climate Report 2025,” the U.S. experienced its costliest wildfire season on record (more than $41 billion) and third-costliest severe convective storm season on record (more than $51 billion).

While tropical cyclone activities were significantly reduced in 2025 because the U.S. mainland went without a landfalling hurricane for its first season in 10 years, flash flood events affected communities in Texas, New York, Florida, New Mexico, Wisconsin, Washington and California.

Speak with a friendly agent and get your quote in minutes!

When does weather damage total a car — and how does the math work?

Insurers declare a vehicle a total loss when the cost to repair it exceeds a particular threshold (usually 70% or 80% of the car’s actual cash value; details vary by state and insurer). Flooding and wildfire have the highest total-loss rates because electrical system damage often makes repairs impractical.

A vehicle’s actual cash value is its market value at the time of loss. This figure reflects the car’s depreciation over time, not its replacement value, which is the price you paid.

Suppose you have a damaged vehicle with an ACV of $14,000 and a repair estimate of $12,000. The repair cost is 86% of the car’s value, which would be considered a total loss by most insurers.

For flood and hurricane damage, your insurer pays the actual cash value of your vehicle minus your deductible. Because water damage to a car’s electrical system almost always results in a total loss, that payout is effectively your vehicle’s market value at the time of the storm. For a car worth $20,000 with a $500 deductible, the settlement check would be approximately $19,500.

If the balance on your auto loan exceeds the vehicle’s ACV, gap insurance could cover the difference.

Check your deductible now: could you afford to pay it? Most deductibles are in the $250 to $1,000 range. Increasing your deductible could help lower your rates, but a deductible that’s too high could be difficult to pay after a damaging storm.

Sophie’s Tip

With electric vehicles, the cost of battery replacement alone can exceed the vehicle’s market value after a flood or fire. That’s why EVs are considered totaled at lower damage thresholds.

How to file a car insurance claim after severe weather — step by step

You should file your weather damage auto claim as soon as it’s safe to do so. Most insurers recommend reporting the claim within 48 hours or even 24 hours if possible. Document the vehicle’s damage with photos and notes before making any permanent repairs, then contact your insurer directly to open the claim. Here is the step-by-step process for filing a claim, from storm to settlement.

- Safety first. Never enter areas with downed power lines and watch for large branches and deep or rushing water. Don’t inspect or start a flood-damaged car, especially if saltwater is involved, as this can cause further engine damage.

- Document damage thoroughly. Take time-stamped photos and video from multiple angles and distances to document damage to the car’s exterior and interior. Also, document your surroundings, including rushing water, fire, smoke or other aftermath damage.

- Report to your insurer within 24 to 48 hours. Have the date, location and your policy number ready. Make sure to call the insurance company directly; don’t go through a third party.

- Hold off on permanent repairs for now. You can make temporary fixes, like covering broken windows with a tarp, but don’t make permanent repairs until the insurance adjuster has taken a look. Save your receipts from all repairs and related costs.

- Meet with the adjuster. Walk them through all vehicle damage and ask for an itemized written estimate.

- Review the settlement offer. If the estimate seems low, you can negotiate it or request a re-inspection. If your claim is denied, request a denial letter to get the reason in writing.

- Choose a repair shop. Your insurer may have a preferred network or repair facilities, but in most states, you have the right to choose your own.

Most repairable weather claims can be resolved within a few weeks, whereas total-loss determinations typically take longer.

For example, in Texas, the insurer must acknowledge the claim within 15 calendar days and has 15 business days to accept or reject it. After accepting your claim, the insurer has five business days to pay. If the damage results from a declared catastrophe, the insurer may have a 15-day extension.

Sophie’s Tip

Before you call your insurer, make sure your photos include the VIN plate, the vehicle’s surroundings, and any storm-related debris still near the car. Adjusters use context, not just close-ups — a photo showing a downed tree next to your dented hood is more useful than a close-up of the dent alone.

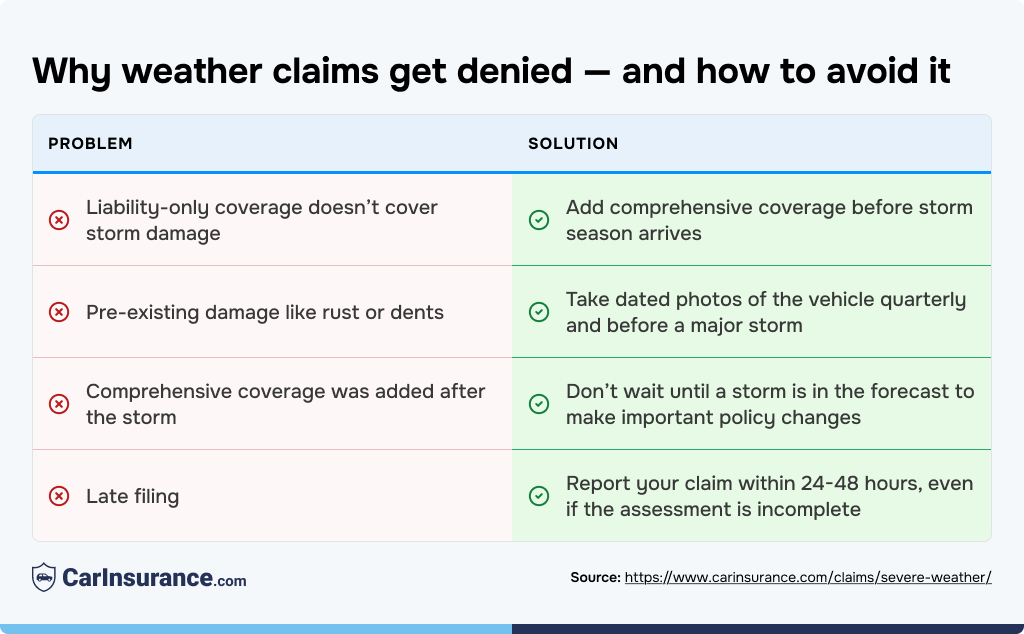

What can get your weather damage claim denied — and how to prevent it

Weather damage claims are denied for four main reasons: the driver carried liability-only coverage, the damage was deemed pre-existing, comprehensive coverage was added after the storm or the claim was filed too late. However, you can avoid these problems if you act now, before a storm hits. Here’s how to help ensure your claim is accepted.

If the insurer denies your claim, request a written reason for the denial. You have the right to appeal the decision or escalate your case to your state’s Department of Insurance.

Will filing a comprehensive claim raise your car insurance rates?

Filing a single weather-related comprehensive claim won’t typically raise your rates the way an at-fault accident does, because weather-related events are outside your control. However, filing multiple claims in a short window could affect your rate at renewal. So could a pattern of weather claims in a high-risk ZIP code.

When claims volume spikes in a geographic area, all policyholders in that ZIP code could see rate adjustments at renewal, not just people who filed claims.

Regarding multiple claims, the general industry practice is to allow a maximum of two or three comprehensive claims within 24 months. More than that will likely prompt an insurer review of your insurance record, regardless of whether you were at fault for the claims.

Motor vehicle insurance costs rose 6% on average in 2025, according to Consumer Price Index data, although the rate of increase slowed to 2.8% year-over-year by December.

The best way to avoid a rate increase is to compare quotes as soon as your claim settles. That way, higher rates aren’t locked in at your current insurer.

How much does comprehensive coverage cost — and is it worth it?

Comprehensive coverage averages $451 annually across the U.S. But the cost of comprehensive coverage more than offsets the cost of a claim after a severe weather event.

For instance, in 2021, a single hail claim in Texas cost more than $5,700 — often more than a full year of comprehensive premiums. For most drivers in states where severe weather is a significant risk, the coverage math is straightforward.

Budget-conscious drivers often skip buying comprehensive coverage. However, if you live in a weather-exposed state, it often makes more sense to buy it, since you’re more likely to file a claim — and the cost is likely to exceed a year’s worth of premiums.

GEICO offers the cheapest comprehensive coverage that’s available. USAA offers lower rates, but coverage is available only to qualifying service members and their families.

Sophie’s Tip

If your car is less than 10 years old and you are in a hail belt or hurricane corridor, the math on comprehensive is usually not close. One covered claim can repay several years of premiums. The question is not whether comprehensive is worth it — it is whether you can absorb a total loss without it.

Read more: What are the most expensive car insurance claims ever

Frequently Asked Questions: Severe weather and car insurance claims

Does car insurance cover all types of weather damage?

Car insurance only covers weather damage if you have comprehensive coverage. It covers hail, flooding, hurricane wind and debris, tornadoes, wildfires, falling trees and ice damage. A liability-only policy doesn’t cover any of these, leaving you to pay for repairs out of pocket. Review your declarations page to confirm your coverage types before storm season.

What is the difference between comprehensive and collision for storm damage?

Comprehensive covers storm damage, such as hailstorm dents or hurricane flooding. Collision pays when your car hits something, such as another vehicle or someone else’s property. If you skid on ice and collide with another vehicle, you’d file a collision claim. If a tornado lifts your car, you’d file a comprehensive claim. Each carries a separate deductible.

Can I add comprehensive coverage right before a storm?

No, not once a storm watch or warning is issued. You’ll need to have coverage in place before a weather event. Most insurers impose a binding restriction (a temporary freeze on coverage additions) when a storm is named or a severe weather watch is active. Add comprehensive coverage to your vehicle before June 1 for hurricane season or before spring for hail season.

How long does a weather damage car insurance claim take?

It varies by state and insurer. For example, Texas law requires insurers to acknowledge claims within 15 calendar days, accept or reject within 15 business days and pay within five business days of acceptance. Most states have similar frameworks. High-volume weather events — a major hurricane or regional hailstorm — can extend timelines as adjusters work through a surge of claims.

Does filing a weather damage claim raise my car insurance rates?

Filing a single comprehensive claim for weather damage rarely triggers a surcharge. Most insurers understand that weather events are outside your control (although multiple claims in a short time will typically trigger a review). The bigger risk is when your area experiences high claim volume after a single major event. In that case, all policyholders are more likely to see a rate increase at renewal.

What should I do immediately after a storm damages my car?

Once it’s safe, take photos and video of the vehicle and your surroundings from every angle. Report it to your insurer within 24-48 hours. Don’t start the car or make any permanent fixes until the adjuster has inspected it. Keep all receipts for any temporary fixes, like covering windows with a tarp.

Is flood damage covered by standard car insurance, or do I need separate flood insurance?

Your standard comprehensive auto policy covers flood damage to your car, so you do not need a separate flood insurance policy for it. FEMA’s National Flood Insurance Program or private flood insurance covers your home, not your car.

Resources & Methodology

Sources

- California Department of Insurance. “California’s public consumer claims tracker continues to show progress in wildfire claim amounts, payments and auto claims.” Accessed May 2026.

- Carrier Management. “State Farm Paid a ‘Hail’ of a Lot of Claims in 2025.“Accessed May 2026.

- Diminished Value of Georgia. “Hail Damage? Why Your ‘Repaired’ Car Is Still Worth 30% Less.”Accessed May 2026.

- Federal Emergency Management Agency (FEMA). “FEMA might help with storm-related vehicle damage.” Accessed May 2026.

- Florida Office of Insurance Regulation. “Hurricane Ian.” Accessed May 2026.

Get advice from an experienced insurance professional. Our experts will help you navigate your insurance questions with clarity and confidence.

Browse all FAQs