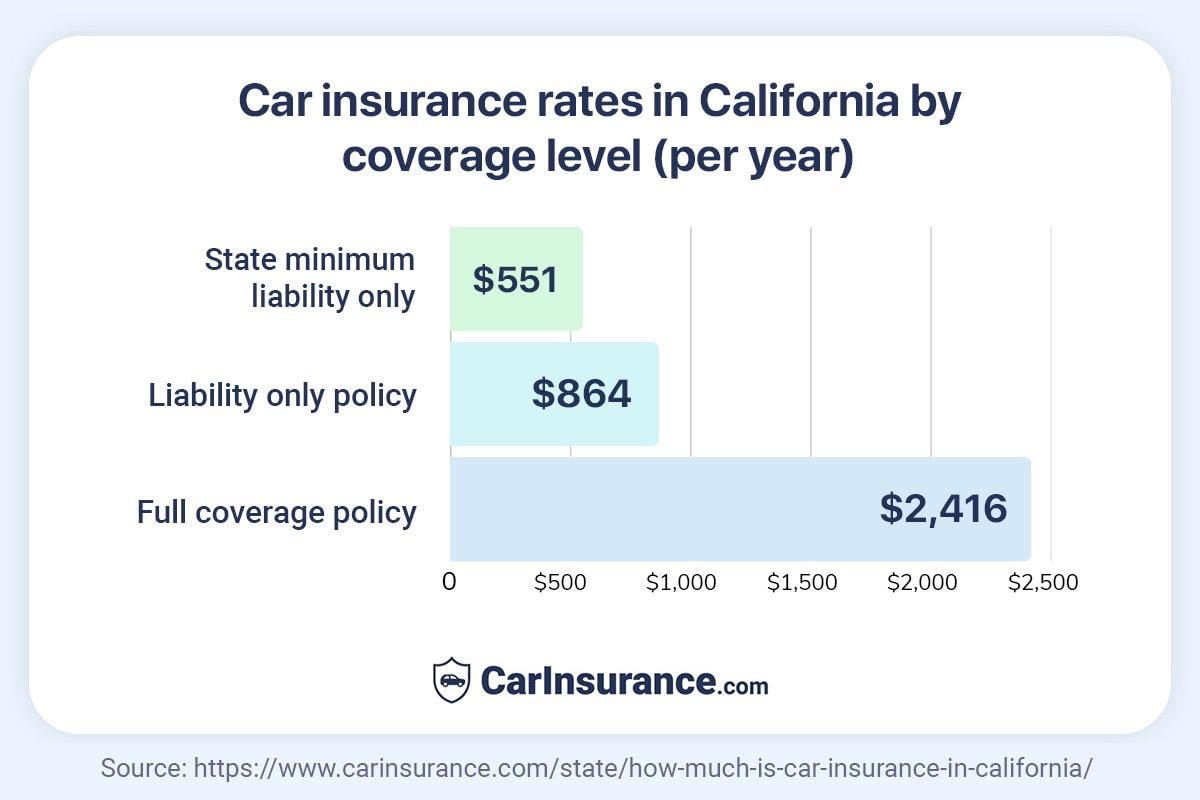

- The average cost of car insurance in California is $2,416 a year or $201 per month, based on our data analysis.

- Minimum liability coverage in California costs around $551 annually for limits of 15/30/5, while liability-only coverage costs $864 per year for limits of 50/100/50.

- Geico provides the most affordable annual rates for full coverage car insurance in California, costing $1,919 per year.

- In California, driving incidents can significantly increase premiums, with a speeding ticket raising rates by up to 43%, a DUI raising rates by 177%, and an at-fault accident by up to 78%.

Car insurance costs in California vary greatly depending on various factors, including the type of coverage you choose, coverage limits, your address and personal factors. Geico offers the cheapest annual rates for full coverage car insurance in California at $1,919 annually.

This comprehensive guide to buying car insurance for California drivers is based on data research and expert advice from CarInsurance.com’s team of insurance analysts and editors. We spent countless hours doing the homework for you and analyzed rates for various driver demographics to show you what you can expect to pay.

Keep reading to learn how auto insurance in California works and how much insurance you need.

How much is car insurance in California?

According to CarInsurance.com data, drivers in California pay about $201 per month for full coverage car insurance.

Understanding the average insurance cost can help you budget effectively for your coverage. Remember that insurance premiums can differ significantly based on your vehicle’s make and model and your driving history.

See how rates change in California based on driver profile:

- Teen drivers in California pay the most — about $519 a month or $6,233 a year.

- Young drivers in their 20s pay an average of $302 monthly or $3,622 annually, for car insurance.

- Senior drivers pay around $202 monthly or $2,424 a year.

- A speeding ticket can increase your rates to $298 monthly or $3,576 annually.

- An at-fault accident increases car insurance rates to $354 a month or $4,246 a year.

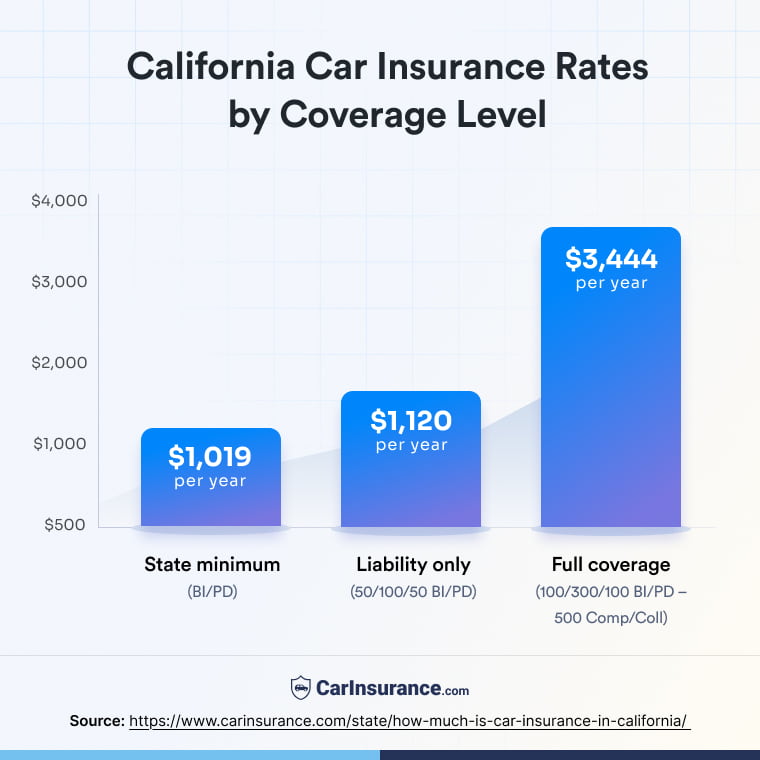

Average cost of auto insurance in California by coverage level

Car insurance costs in California can differ based on the coverage limit. To legally drive, California residents must adhere to the minimum liability limits of 15/30/5.

Liability-only policies are the cheapest, offering bare-bones protection that meets state’s financial responsibility laws – but they don’t offer much legal protection and coverage for your medical costs or property damage.

While liability insurance protects you from financial loss by covering legal defense and damages if you’re found responsible for causing injury or property damage to others, it doesn’t protect your vehicle or passengers.

Full coverage car insurance policies are the most expensive but provide much more protection. They cover your own vehicles from accidents, theft, natural disasters and animal strikes. With a full-coverage insurance policy, drivers can be confident that they’re protected in the event of an accident up to the limits of their policies.

Full coverage comprises liability, comprehensive, collision and any other coverage required by your state.

Below are the California car insurance costs for three different coverage levels.

| Coverage level | Monthly rates | Annual rates |

|---|---|---|

| State Minimum BI/PD | $85 | $1,019 |

| Liability Only – 50/100/50 BI/PD | $93 | $1,120 |

| Full Coverage – 100/300/100 BI/PD – 500 Comp/Coll | $287 | $3,444 |

State minimum car insurance in California

California’s car insurance laws require a minimum coverage of $15,000 in bodily injury liability per person, $30,000 in bodily injury liability per accident and $5,000 in property damage liability.

The state minimum car insurance cost in California is $551 a year. However, this basic coverage only offers limited protection. California drivers can choose to add more coverage, such as comprehensive and collision insurance, raise their liability limits and include personal injury protection or other insurance coverage, for better protection.

Drivers in California must purchase the minimum required car insurance to operate their vehicles on the road.

Liability-only car insurance in California

According to CarInsurance.com data, liability-only car insurance costs $864 in California for limits 50/100/50.

This policy covers the cost of damages caused to others but not damages to the policyholder’s vehicle or passengers. While it is less expensive than a full coverage plan, liability-only insurance does not protect against an accident or theft of the insured vehicle.

Full coverage car insurance in California

In California, you can expect to pay around $2,416 per year for full coverage car insurance for the limits of 100/300/100 – $100,000 in bodily injury coverage, $300,000 in bodily injury coverage per accident and $100,000 in property damage coverage.

Car insurance experts advise drivers to get full coverage insurance with the highest liability limits they can afford. Full coverage includes liability, comprehensive and collision coverage, with a deductible.

Calculate the cost of car insurance in California

A policy that is perfect for someone living in one ZIP code might be expensive for a driver living in another.

Different areas pose more or less risk based on crime rate, traffic, car thefts and population density. Insurance companies research each area’s risks and then use that information to determine what they can charge for premiums.

As a result, people living in higher-risk neighborhoods of California have to pay more than those living where the risks are lower.

With our easy-to-use tool, you can get insurance quotes for different coverage limits for your ZIP code in minutes. Enter your ZIP code into our free tool to see how much you can save.

Calculate car insurance rates by ZIP code in California

Rates vary by location. Our tool helps you understand how your ZIP code impacts your premium.

For 30 year old Male ( Full - 100/300/100)

Speak with a friendly agent and get your quote in minutes!

Estimate car insurance in California by car model

Car insurers in California use the make and model of your car to determine your insurance rates. Cars deemed more expensive to repair, such as luxury cars and EVs, may raise your rates more than those that may cost less to fix.

For instance, Maserati, BMW, Porsche and Audi are some of the most expensive cars to insure. Subaru, Hyundai, Honda and Mazda are among the cheapest cars to insure.

See how much you’ll pay for car insurance for your specific make and model in California.

Insurance rates by car model

Guide: How to estimate car insurance using our car insurance estimator tool

Car insurance rates by age group in California

Younger drivers and teenagers typically pay more for insurance than older, more experienced drivers. This is because teenagers are more likely to get into car accidents. In fact, teenagers are four times more likely to crash than drivers who are 20 or older, according to the Insurance Institute for Highway Safety.

Insurers know that teenage drivers are less experienced and pose a higher risk, resulting in higher insurance premiums. California drivers between the ages of 30 to 60 typically enjoy the lowest average auto insurance rates, at about $2,392 annually.

Car insurance for drivers aged 16-19 costs $3,841 more annually than California drivers aged 30-60.

See the average rates by age group below:

- For teen drivers: Teens aged 16-19 can expect to pay $6,233 per year for a full coverage car insurance policy.

- For young adults: Drivers aged 20-25 can expect to pay $3,509 a year for a full coverage policy.

- For average-aged drivers: Drivers aged 30 to 60 can expect to pay $2,392 per year in California.

- For senior drivers: Drivers age 65 and older can expect to pay $2,424 per year.

Check out our detailed guide on average car insurance rates by age

Rates based on driver profile, history and habits in California

Having a DUI, speeding ticket or being at fault in an accident can substantially increase your insurance rates. In California, a DUI conviction often results in higher premiums and you may see an increase of up to 177% as insurers perceive you as a high-risk driver.

If you get caught speeding in California, your car insurance rates will increase by 43% when you renew your policy. Typically, you’ll pay the increased premiums for three years. But how much your rates go up can vary depending on the laws in your state, the insurance company you’re with, and your driving history.

Here’s a breakdown of how much your car insurance rate goes up in California following driving incidents:

- Speeding ticket: Up to 43% increase

- DUI conviction: 177% increase

- At-fault accident (bodily injury and property damage): 78% increase

Even if you’ve received a traffic ticket, comparing quotes can still help you save money.

Car insurance cost in California for high-risk drivers

High-risk drivers in California pay more for car insurance than other drivers because they are considered riskier. Factors like accident history, traffic violations and poor credit scores influence how much the policyholder will pay for insurance coverage.

Luckily, there are ways for high-risk drivers to reduce their premium payments. Shopping around and comparing quotes is a great place to start, as each company will have its own rate structure tailored to individual needs.

Use the tool below to see which company offers cheaper rates for drivers with speeding tickets, DUI convictions and at-fault accidents.

Select your state and risk factor below to see the insurance company and its average annual full coverage rates.

Learn more: The 10 most important factors that affect car insurance rates

Explore car insurance costs in your neighboring states

Compare car insurance quotes in California

In California, drivers can save on car insurance by comparing prices from different companies. Many factors affect how much you pay, like your driving history and the type of car you drive. Luckily, there are plenty of choices to help you find good insurance that fits your budget.

Compare the best car insurance options in California by getting quotes from different insurance companies.

Below are the details of California car insurance companies and their annual premiums.

| Company | State Minimum | 50/100/50 | 100/300/100 |

|---|---|---|---|

| GEICO | $565 | $625 | $2,039 |

| Mercury Insurance | $866 | $944 | $2,786 |

| CSAA Insurance (AAA) | $541 | $570 | $2,877 |

| Progressive | $624 | $673 | $3,013 |

| Auto Club Enterprises (AAA) | $1,027 | $1,107 | $3,559 |

| Allstate | $1,374 | $1,436 | $4,032 |

| Nationwide | $1,433 | $1,644 | $4,164 |

| State Farm | $1,260 | $1,437 | $4,171 |

| Farmers | $1,562 | $1,733 | $4,486 |

Car insurance rates by city in California

Tarzana is the most expensive city in California, with an average car insurance rate of $3,430 a year. Mount Shasta is the cheapest city for California drivers at an average rate of $1,832 annually.

Car insurance rates vary by city in California for several reasons. One of the most significant factors is traffic congestion. Areas with more traffic typically have higher rates of accidents and claims, which leads to higher premiums.

Other factors that can affect rates include the number of uninsured drivers, the cost of repairs and medical bills and the crime rate in the city.

Below, you’ll see the average annual car insurance cost of major cities in California.

Select your city below to see the insurance company and its average full coverage rates.

How much does car insurance cost in California per month?

In California, a full coverage car insurance policy with 100/300/100 limits typically costs about $201 per month.

Opting for monthly car insurance payments can be a budget-friendly strategy for some people. It allows for spreading the cost throughout the year, making it easier to manage than a hefty annual payment. This approach provides more flexibility and avoids the burden of a large upfront sum.

Alternatively, paying your car insurance in full upon renewal may earn you a discount. Ultimately, the ideal choice depends on your needs and situation.

| Coverage level | Monthly rates |

|---|---|

| State Minimum BI/PD | $85 |

| Liability Only – 50/100/50 BI/PD | $93 |

| Full Coverage – 100/300/100 BI/PD – 500 Comp/Coll | $287 |

Final thoughts on choosing car insurance in California

There’s no one best car insurance for everyone. Some drivers are willing to pay a bit more for outstanding customer service, some want the lowest rates, others prefer carriers who can handle claims and payments through mobile apps and some prefer agents.

Ultimately, understanding your needs to find the best policy at the most competitive price is critical. Shop around for a good deal that provides peace of mind when hitting the open road in California.

Resources & Methodology

Sources

- Insurance Institute for Highway Safety. “Teenagers.” Accessed April 2026.

- USAA. “How credit affects insurance premiums.” Accessed April 2026.

Methodology

CarInsurance.com commissioned Quadrant Information Services to get car insurance rates in California. The average premiums are based on the sample profile of a 40-year-old male and female driving a Honda Accord LX with a good insurance score and a clean driving record.

The rates are for different coverage limits. It includes:

- Full coverage car insurance with a coverage limit of $100,000 in bodily injury per person, $300,000 in bodily injury coverage per accident, $100,000 in property damage coverage per accident and a $500 collision/comprehensive deductible.

- Liability-only car insurance rates with a limit of 50/100/50.

- State minimum coverage limit of 15/30/5.

Read the detailed methodology for more information.

Note: USAA is only available to military community members and their families.

Get advice from an experienced insurance professional. Our experts will help you navigate your insurance questions with clarity and confidence.

Browse all FAQs