CarInsurance.com Insights

- A car is totaled when repair costs exceed 70-80% of its value, but thresholds vary by state.

- Insurers often deny buyback requests due to the risk associated with driving a previously totaled car. Even if repairs are possible, there is no guarantee that the vehicle will be restored to a safe and reliable condition.

- If your insurer denies, accepting the full ACV settlement will help you get a replacement vehicle. You can also appeal by checking your state DMV rules, bringing your own repair estimates or questioning the insurer’s reasons for denying the buyback request.

Insurers can deny a retention request if the vehicle poses a safety risk, if state salvage laws don’t allow policyholders to keep totaled vehicles or if the insurer determines that allowing the car back on the road creates excessive liability.

When insurers approve buybacks, they deduct the salvage value from your actual cash value (ACV) payout, and the car is returned to you with a salvage title, which affects how you can register and insure it going forward.

This guide explains how the buyback process works and what other options you have.

What does it mean when your car is totaled?

Your car is considered totaled when your insurance company determines that the cost to repair it exceeds a set percentage of the car’s pre-accident value, typically between 70% and 80%, depending on your state. Once declared totaled, you’ll receive the car’s ACV, and your insurer will take ownership of it.

Insurers apply the total-loss formula, or TLF, to determine whether a vehicle is a total loss. If the estimated repair costs, when compared to the car’s actual cash value, reach or exceed the threshold set by your state, the vehicle is considered totaled.

Total Loss Formula: Repair costs + salvage value ≥ actual cash value (ACV)

Once a total loss is declared, your insurer issues a salvage title for the vehicle. A salvage title is a permanent part of the car’s history, indicating it sustained significant damage. It affects the car’s resale value, your ability to insure it again and, in some states, whether you can legally drive it on public roads.

A totaled car isn’t necessarily undrivable; it simply means the math didn’t work out in favor of a repair. Since each state sets its own total loss threshold, an accident that results in a totaled vehicle in one state might be repairable in another.

Can you keep your totaled car?

In most states, you can request to keep your totaled car by accepting a reduced insurance payout. The insurer deducts the salvage value and transfers the salvage title to you. However, some states outright prohibit retention, and insurers may still deny the request for safety reasons or due to state laws.

Once you keep a totaled car, you cannot legally drive it until it’s repaired and passes a state inspection for a rebuilt or reconstructed title. Most insurers will only offer liability coverage for a salvage-titled vehicle, not comprehensive or collision coverage.

How to buy back your totaled car from your insurance company

To buy back your totaled car, notify your insurer of your intent before the settlement is finalized. The insurer will deduct the vehicle’s salvage value from your payout, issue you a salvage title and return the car to you.

Here’s how the buyback a totaled car process works, step by step:

- Step 1: Act fast and notify your insurer: As soon as your car is declared a total loss, tell your claims adjuster you want to retain the vehicle. Do this verbally and follow up in writing.

- Step 2: Get the salvage value estimate: Your insurer will calculate the salvage value, which is deducted from your actual cash value (ACV) payout. For example, if your car’s ACV is $12,000 and salvage value is $2,500, you’d receive $9,500.

- Step 3: Confirm your state allows retention: Not every state permits policyholders to keep a totaled car. Illinois, for instance, requires the insurer to take possession of a vehicle once it is declared a total loss. Check your state’s DMV or insurance department website before assuming the option is available to you.

Sophie’s Interesting Facts

You can only retain your totaled vehicle in Illinois if:

- The car has sustained only hail damage that does not affect its operational safety.

- The vehicle is nine (9) model years old.

- Step 4: Negotiate if the salvage deduction seems high: Salvage value estimates vary. If you believe your insurer’s figure is inflated, you can request documentation of how it was calculated or get your own estimate from a licensed dealer.

- Step 5: Accept the settlement and sign the title: Once you agree on the salvage deduction, the insurer will then issue you a salvage title, which legally brands the vehicle as totaled.

- Step 6: Repair the car and get a rebuilt title: A salvage-titled car cannot be legally driven on public roads in most states. You’ll need to have it repaired, then pass a state inspection to receive a rebuilt title.

- Step 7: Get insurance for a rebuilt-title vehicle: Insuring a rebuilt-title car is more complicated than insuring a standard vehicle. Specialty insurers and some regional carriers do offer broader coverage after an independent inspection confirms the vehicle is roadworthy.

Why would drivers want to keep their totaled cars?

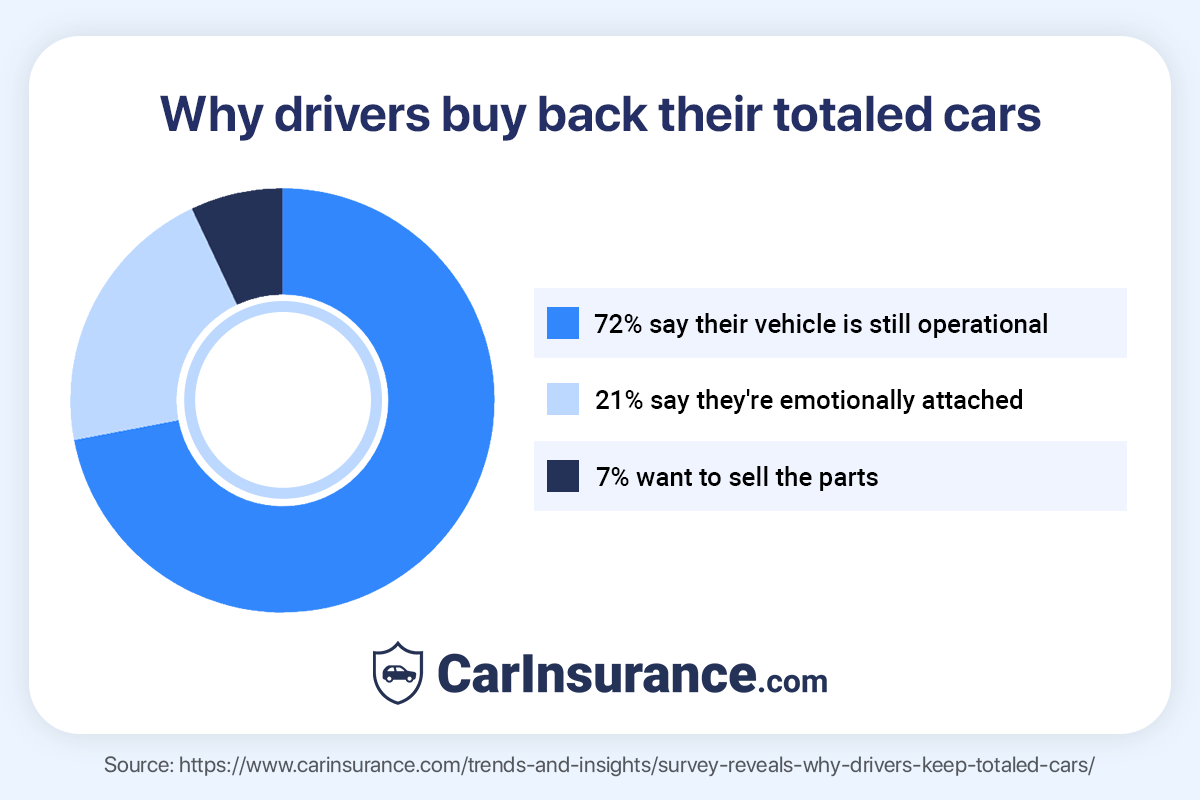

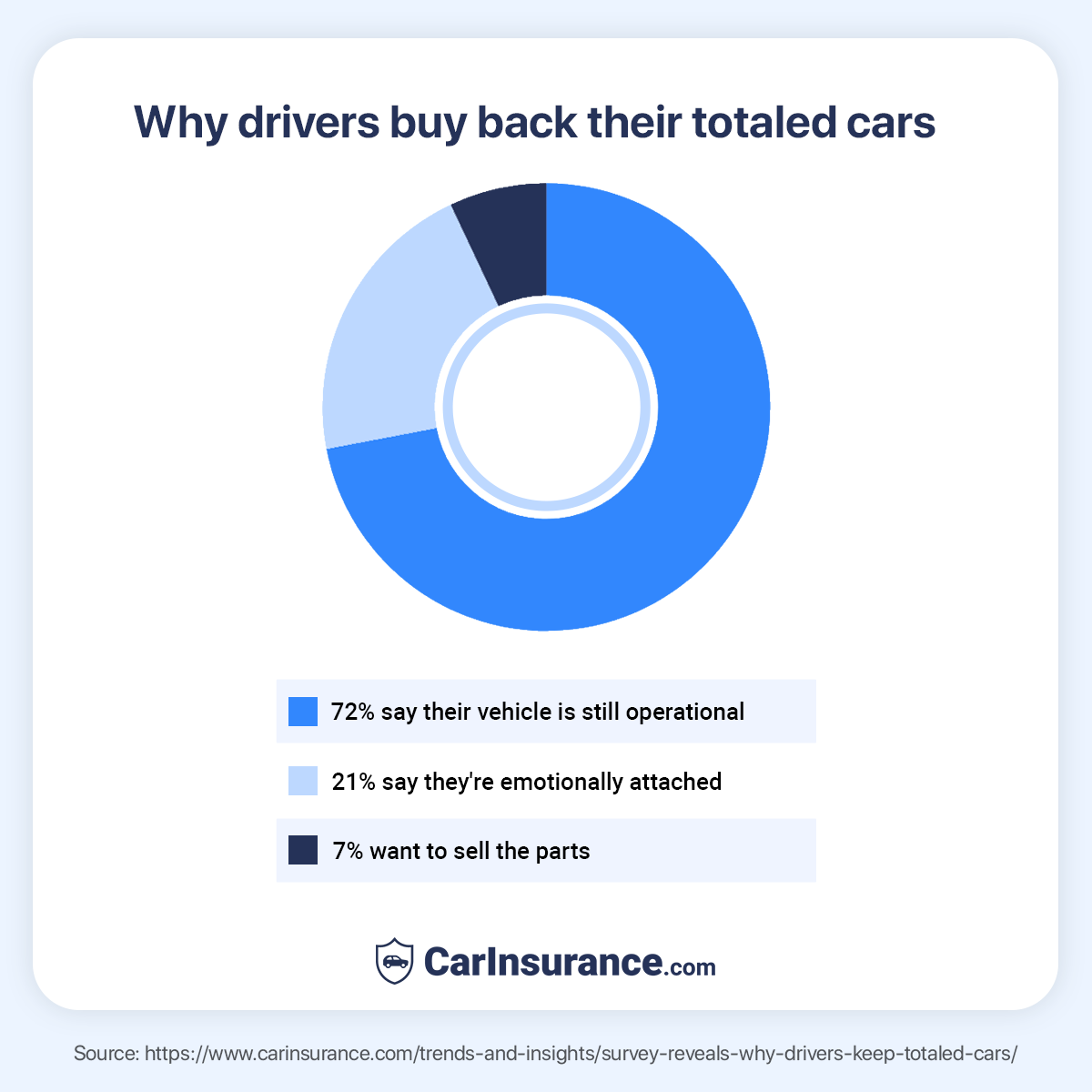

Insurers don’t always allow buybacks after a vehicle is totaled, but many drivers want to keep their cars. A CarInsurance.com poll found that 72% of respondents would repurchase their totaled car if it were still operational, while 21% said they kept their totaled car due to an emotional attachment.

Even if a vehicle can be repaired, insurance companies may refuse to sell it back due to salvage-title laws or the possibility that the car could return to the road in an unsafe condition.

Speak with a friendly agent and get your quote in minutes!

What are your options if the buyback request is denied?

If an insurance company refuses your request to keep the totaled vehicle, consider exploring alternatives.

- Buy a replacement vehicle. Use your settlement to purchase a similar car with the compensation from your insurer. It ensures you have a reliable, safe mode of transportation. Consider repairing the car independently to ensure all safety standards are met.

- Appeal the total loss decision: If you believe your car shouldn’t have been totaled or that the ACV is too low, you can formally dispute the settlement. Most auto insurance policies let you hire an independent appraiser.

- Buy the car at an auction: Even if your insurer won’t sell the car back to you, the vehicle will likely go to a salvage auction, and you can bid on it there.

Frequently asked questions: Buying back totaled cars

Can I insure a car with a salvage title?

Yes, you can insure a car with a salvage title, but your options may be limited. A salvage title means the vehicle was totaled by an insurance company, usually due to significant damage. Because totaled vehicles are considered high-risk, many insurance companies offer only limited coverage.

Even when full coverage is available, insurers may require a detailed inspection and photos of the vehicle, and the payout in the event of a claim will be based on the car’s reduced market value.

Do I have to accept my insurer’s total loss settlement?

No, you do not have to automatically accept your insurer’s totaled vehicle settlement if you believe it is too low. When a vehicle is declared a total loss, the insurance company is required to pay you the car’s actual cash value (ACV) at the time of the loss, which is based on factors such as its age, mileage, condition and comparable vehicle sales in your area.

If you disagree with the amount offered, you have the right to review the valuation report, check the comparable vehicles used and provide your own evidence, such as recent maintenance records, receipts for upgrades or listings of similar vehicles priced higher.

What’s the difference between a salvage title and a rebuilt title?

The main difference between a salvage title and a rebuilt title is the vehicle’s condition and legal status for driving. A salvage title is issued when a car has been declared a total loss by an insurance company due to significant damage from an accident, flood, fire or other event. At this stage, the vehicle is generally not considered safe to drive and cannot be legally registered or operated on public roads until it is repaired.

A rebuilt title, on the other hand, is issued after a salvage vehicle has been repaired and has passed a state inspection confirming it meets safety requirements. While a rebuilt vehicle can be legally driven and insured, it typically has a lower market value. It may still be harder to insure compared to a vehicle with a clean title.

Will my insurance payout cover what I still owe on the car?

When your car is declared a total loss, your insurance company will typically pay the vehicle’s actual cash value at the time of the accident, which reflects its depreciated market value, not the amount you still owe on your loan or lease.

It’s possible to owe more than the insurance payout covers because cars often depreciate faster than loan balances decrease. If that happens, you would be responsible for paying the remaining balance out of pocket unless you have gap insurance.

Sources

- Kelley Blue Book. “Totaled Car” Accessed February 2026.

- Illinois Department of Insurance. “Illinois Insurance Facts.” Accessed February 2026.

Get advice from an experienced insurance professional. Our experts will help you navigate your insurance questions with clarity and confidence.

Browse all FAQs