CarInsurance.com Insights

- The cheapest sedan to insure is the Subaru Legacy with an annual premium of $2,529.

- Travelers and GEICO offer the cheapest rates for sedans.

- Sedans are typically more expensive to insure than SUVs but less expensive to insure than sports cars.

If you’re shopping for a sedan, you must budget for more than just a car payment. You should know how much it will cost to insure the car and where you can find the cheapest car insurance.

However, finding the cheapest insurance isn’t always easy – there are many sedan models and styles, and consumers should be aware that premiums vary depending on different features.

The number of variables factored into your car insurance rate can make your head spin, says Chris Hardesty, an insurance expert and senior advice editor for Kelley Blue Book.

“Driver-assist technologies can make your car safer on the road and potentially avoid a crash,” Hardesty says. “At the same time, those electronic features are more expensive to repair or replace following an accident. It’s good that insurance companies have tremendous amounts of data to help them predict risk and cost.”

What are the cheapest sedans to insure?

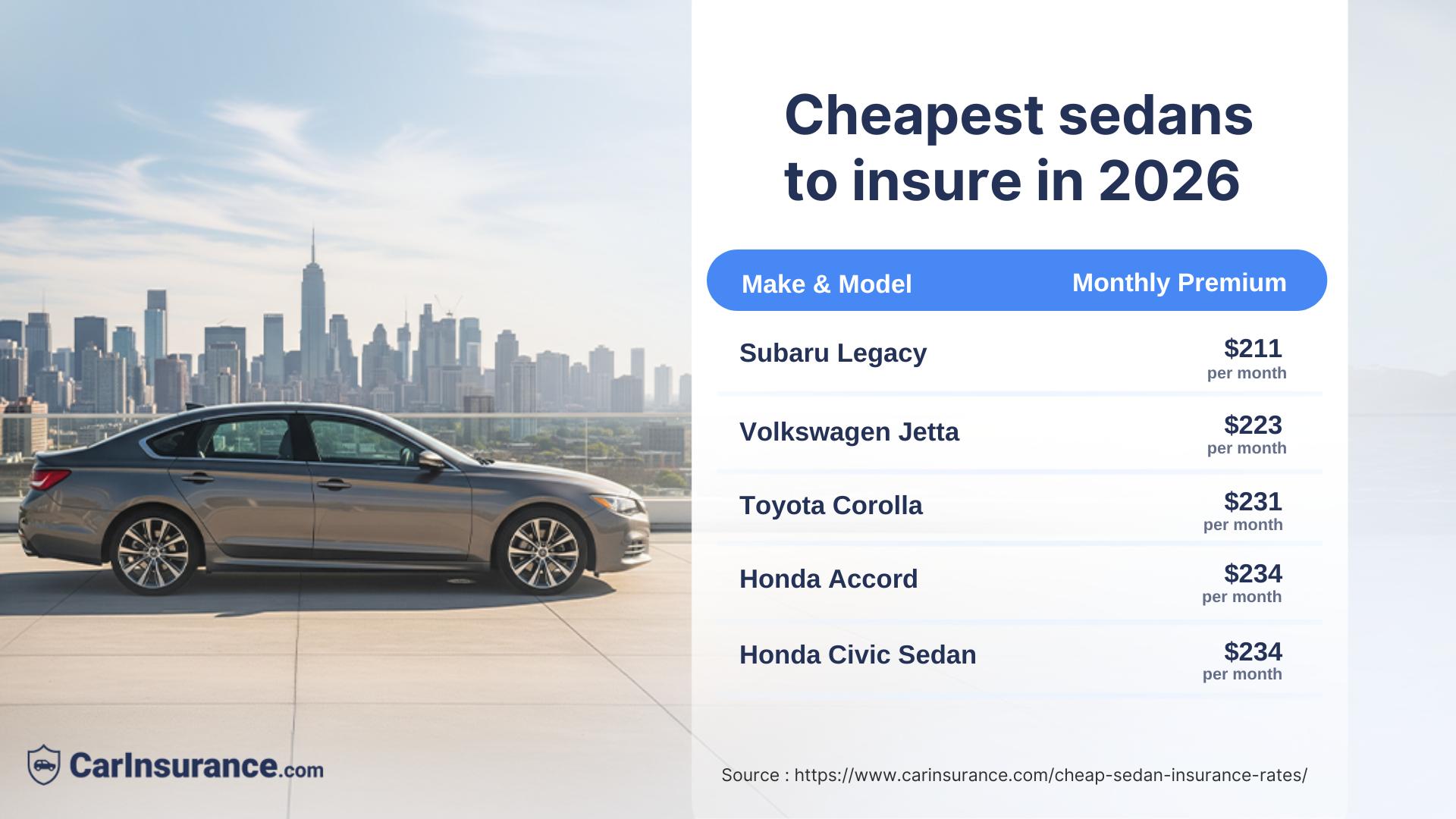

The Subaru Legacy is the cheapest sedan to insure at an average annual premium from Nationwide at $2,529, according to CarInsurance’s data. Nationwide also had the second-lowest rates for the Subaru Impreza.

No. 1: Subaru Legacy

- Cost: $2,529 per year; $211 per month

No. 2: Volkswagen Jetta

- Cost: $2,677 per year; $223 per month

No. 3: Toyota Corolla

- Cost: $2,771 per year; $231 per month

No. 4: Honda Accord

- Cost: $2,804 per year; $234 per month

No. 5: Honda Civic

- Cost: $2,809 per year; $234 per month

Which companies provide the cheapest car insurance for sedans?

Travelers offers the cheapest car insurance rates for sedans, starting at an annual average premium of $1,763 for a Subaru Legacy. Learn how other insurance companies’ annual premiums rank in the table below.

| Make model | Company | Annual rates | Six-month rates | Monthly rates |

|---|---|---|---|---|

| Subaru Legacy | Travelers | $1,763 | $882 | $147 |

| Volkswagen Jetta | Travelers | $1,988 | $994 | $166 |

| Mazda 3 | Travelers | $1,993 | $997 | $166 |

| Honda Accord | Travelers | $2,013 | $1,007 | $168 |

| Nissan Versa | GEICO | $2,045 | $1,023 | $170 |

| Volkswagen Jetta GLI | Travelers | $2,050 | $1,025 | $171 |

| Toyota Corolla | GEICO | $2,073 | $1,037 | $173 |

| Honda Civic | Travelers | $2,184 | $1,092 | $182 |

| Hyundai Sonata | Travelers | $2,299 | $1,149 | $192 |

| Chevrolet Malibu | GEICO | $2,313 | $1,156 | $193 |

| Kia K4 | Travelers | $2,316 | $1,158 | $193 |

| Hyundai Elantra | Travelers | $2,317 | $1,159 | $193 |

| Nissan Sentra | GEICO | $2,341 | $1,171 | $195 |

| Nissan Altima | Travelers | $2,411 | $1,205 | $201 |

| Kia K5 | Travelers | $2,437 | $1,219 | $203 |

Do insurance companies consider the vehicle size when setting rates?

Yes. When determining premiums, car insurance companies typically consider the type of car you drive, its cost, potential repair costs and theft. Additionally, they assess safety features, potential damage to another car during an accident and luxury model features.

According to our data, drivers of a small Toyota Corolla can estimate an average annual premium of $2,771. Comparatively, drivers of a midsize Honda Accord have an average annual premium of $2,804, a difference of $33. Drivers of a full-size Hyundai Sonata can see an increase of nearly $300 with an average annual premium of $3,097 for full coverage car insurance.

See the tables below to further compare premiums, insurance companies and sedan size.

Cheapest small sedans to insure

According to our analysis, the Volkswagen Jetta is the cheapest small sedan to insure through Travelers. The table below shows what other insurance companies offer the cheapest coverage for sedans.

| Make model | Company | Annual rates | Six-month rates | Monthly rates |

|---|---|---|---|---|

| Volkswagen Jetta | Travelers | $1,988 | $994 | $166 |

| Mazda 3 | Travelers | $1,993 | $997 | $166 |

| Volkswagen Jetta GLI | Travelers | $2,050 | $1,025 | $171 |

| Toyota Corolla | GEICO | $2,073 | $1,037 | $173 |

| Honda Civic | Travelers | $2,184 | $1,092 | $182 |

| Kia K4 | Travelers | $2,316 | $1,158 | $193 |

| Hyundai Elantra | Travelers | $2,317 | $1,159 | $193 |

| Nissan Sentra | GEICO | $2,341 | $1,171 | $195 |

Cheapest midsize sedans to insure

The Subaru Legacy is the cheapest midsize sedan to insure through Travelers, according to our data. Learn more about the cheapest midsize sedans to insure in the table below.

| Make model | Company | Annual rates | Six-month rates | Monthly rates |

|---|---|---|---|---|

| Subaru Legacy | Travelers | $1,763 | $882 | $147 |

| Honda Accord | Travelers | $2,013 | $1,007 | $168 |

| Hyundai Sonata | Travelers | $2,299 | $1,149 | $192 |

| Chevrolet Malibu | GEICO | $2,313 | $1,156 | $193 |

| Nissan Altima | Travelers | $2,411 | $1,205 | $201 |

| Kia K5 | Travelers | $2,437 | $1,219 | $203 |

Cheapest full-size sedans to insure

The Toyota Camry is the cheapest full-size sedan to insure through Travelers. Full-size sedans typically don’t rank in the “cheap” category, but you can explore the average rates for them below.

| Make model | Company | Annual rates | Six-month rates | Monthly rates |

|---|---|---|---|---|

| Toyota Camry | Travelers | $2,070 | $1,035 | $172 |

| Hyundai Sonata | Travelers | $2,299 | $1,149 | $192 |

| Chevrolet Malibu | GEICO | $2,313 | $1,156 | $193 |

| Nissan Altima | Travelers | $2,411 | $1,205 | $201 |

Are new or used cars cheaper to insure?

Are new or used cars cheaper to insure?Typically, it’s more expensive to insure a new car than an older one. That’s because a newer vehicle is more valuable, making it more expensive to repair or replace than an older sedan.

Speak with a friendly agent and get your quote in minutes!

What are the car insurance requirements for sedans?

The insurance requirements for sedans are the same as for other types of vehicles. Below are the car insurance options, but keep in mind that these are not all legal requirements, which vary by state:

- Liability: If you injure another person or damage their property while at the wheel of your sedan, bodily injury liability and property damage liability will help cover damages up to your policy’s limits. Liability coverage is required in most U.S. states.

- Collision: If your car is damaged or destroyed after a collision with another car, collision coverage will cover damage.

- Comprehensive: Should your vehicle be damaged or destroyed by something other than a collision – fire, flooding, vandalism, theft, weather events or an animal strike – comprehensive coverage comes to the rescue.

- Uninsured motorist/underinsured motorist: If your car is damaged in a crash with an uninsured or underinsured driver, UM/UIM coverage will help foot the repair bill.

How much you’ll pay for car insurance depends on several factors:

- Insurance company

- Age, make and model of the vehicle

- Address where the vehicle is garaged

- Coverage amounts (the more extensive the coverage, the more expensive)

- Deductible (a higher deductible means a cheaper premium)

- Individual driving history

- State of residency

The cheapest type of insurance for sedans that is currently available is liability-only insurance. But if you’re leasing or financing your car, you need comprehensive and collision insurance and liability insurance.

How has the cost of insurance changed over time?Car insurance costs have continued to climb over the years. In fact, the U.S. Bureau of Labor Statistics reported that insurance rates rose 11.1% over a one-year period ending in early 2025.

How much is insurance for a sedan for an 18-year-old vs. a 40-year-old?

In general, teen drivers pay significantly more for insurance than 40-year-old drivers. As drivers gain experience behind the wheel, they pose less risk for insurers, leading to lower rates.

For example, a 40-year-old driver pays an average annual rate of $2,529 to insure a Subaru Legacy. In contrast, an 18-year-old pays an average annual rate of $8,130 to insure the same vehicle.

Explore how rates vary across other vehicles by driver age below.

| Make model | Annual rates | Six-month rates | Monthly rates |

|---|---|---|---|

| Subaru Legacy | $8,130 | $4,065 | $678 |

| Volkswagen Jetta | $8,820 | $4,410 | $735 |

| Honda Accord | $9,066 | $4,533 | $756 |

| Toyota Corolla | $9,106 | $4,553 | $759 |

| Honda Civic | $9,202 | $4,601 | $767 |

| Mazda 3 | $9,218 | $4,609 | $768 |

| Nissan Versa | $9,474 | $4,737 | $790 |

| Volkswagen Jetta GLI | $9,480 | $4,740 | $790 |

| Chevrolet Malibu | $9,529 | $4,764 | $794 |

| Hyundai Elantra | $9,905 | $4,953 | $825 |

| Nissan Sentra | $9,936 | $4,968 | $828 |

| Hyundai Sonata | $10,129 | $5,065 | $844 |

| Nissan Altima | $10,151 | $5,075 | $846 |

| Kia K5 | $10,385 | $5,192 | $865 |

| Kia K4 | $12,847 | $6,424 | $1,071 |

| Make model | Annual rates | Six-month rates | Monthly rates |

|---|---|---|---|

| Subaru Legacy | $2,529 | $1,265 | $211 |

| Volkswagen Jetta | $2,677 | $1,339 | $223 |

| Toyota Corolla | $2,771 | $1,386 | $231 |

| Honda Accord | $2,804 | $1,402 | $234 |

| Honda Civic | $2,809 | $1,404 | $234 |

| Mazda 3 | $2,817 | $1,408 | $235 |

| Volkswagen Jetta GLI | $2,885 | $1,443 | $240 |

| Nissan Versa | $2,894 | $1,447 | $241 |

| Chevrolet Malibu | $2,897 | $1,448 | $241 |

| Nissan Sentra | $3,013 | $1,506 | $251 |

| Hyundai Elantra | $3,030 | $1,515 | $253 |

| Hyundai Sonata | $3,097 | $1,549 | $258 |

| Nissan Altima | $3,114 | $1,557 | $260 |

| Kia K5 | $3,192 | $1,596 | $266 |

| Kia K4 | $4,017 | $2,008 | $335 |

What leads to higher car insurance costs for sedans?

According to a Kelley Blue Book report, SUVs made up the lion’s share of car sales in the first half of 2022. However, in the first quarter of 2023, sedans saw an uptick in sales, about 21.4% of the 3.6 million new vehicles sold in the U.S., according to the Automotive News Research & Data Center.

This has safety implications since sedans are smaller and lower to the ground than trucks and SUVs.

Here are some factors that lead to a higher insurance cost for sedans:

- Car make and model: The price tag of your insurance hinges on the specific car make and model. Luxury vehicles, larger cars, more powerful engines and models with more bells and whistles mean more expensive car insurance.

- Higher potential for theft: One downside to sedans’ popularity is that they are also attractive to car thieves, Hardesty says. In fact, data by the NICB reveals that five of the top 10 most stolen cars in the U.S. are sedans.

- Cost to repair: Sedans with more features, electronic components or expensive parts will cost more, which will raise the insurance premium.

- Market value: Sedans with a higher market value — or resale value — will have a higher insurance price tag.

- Safety features: Sedans with safety features such as brake assist, airbags, anti-lock brakes and backup cameras can lower the odds of getting into a car crash, decreasing your insurance cost.

How to save money on car insurance for sedans

To save on car insurance, understand that an older car will also be cheaper to insure than a newer luxury model. And the higher your deductible, the lower your premium and vice versa.

Take these steps before buying a car insurance policy for your sedan:

- Research to see what type of coverage you need: As mentioned before, you’ll want to see what types of insurance and coverage amounts you’ll need. Each state has different requirements, and most states require liability. If you are leasing or financing a car, you’ll most likely need full coverage, which includes comprehensive and collision insurance.

- Comparison shop: To save on car insurance for your sedan, it’s important to do your research to get an idea of the rates. Get a few quotes from several lenders for the same types and coverage amounts. The beauty of car insurance is that you can hop on a new policy with a different insurance company at any time.

- Look for discounts: You’ll also want to see if there are any discounts. Common discounts for car insurance include a good driver discount, a membership discount if you’re affiliated with a certain organization, a multi-vehicle discount and bundled discount if you purchase both a homeowners insurance and auto insurance policy with the same company.

Are sedans cheaper to insure than SUVs or sports cars?

No, sedans are more expensive to insure than SUVs. According to our data, an SUV’s average annual insurance premium is $2,976, while a sedan costs $3,781 per year for full coverage.

Why’s that? Well, it has to do with safety considerations.

“Those SUVs and trucks have grown heavier and taller, while sedans are comparatively petite and close to the road,” Hardesty says. “The difference in weight and stature can put sedans at a disadvantage, leading to higher insurance rates.”

However, sedans are significantly cheaper to insure than sports cars. The average annual premium to insure a sports car is $3,880. Again, this boils down to safety features and underlying value.

Sedan car insurance in a nutshell

When shopping around for insurance for a sedan, consider what you use your car for, how often you drive, and your personal budget. If you want cheaper car insurance rates, opt for a used car with less features.

If a luxury model or a sedan with more advanced features is a better fit for your needs and lifestyle, then there’s no reason to deprive yourself — know it will cost more to insure.

Frequently Asked Questions: Sedan car insurance

Do luxury sedans have higher insurance costs than standard sedans?

Yes, luxury cars come with an average annual premium of $3,952. In contrast, standard sedans have an average annual premium of $3,781.

Do four-door sedans have lower insurance rates than two-door cars?

On average, you’ll pay 16% more to insure a coupe (two-door car) than a sedan (four-door car).

Do older sedans have lower insurance rates than new sedans?

Yes, older sedans are typically cheaper to insure than new sedans.

Resources & Methodology

Sources

Kelley Blue Book. “In an SUV World, Can Cars Make a Comeback?” Accessed March 2026 .

Methodology

CarInsurance.com editors collected rates from Quadrant Information Services for a 40-year-old male and female driver carrying a full coverage insurance policy with limits 100/300/100 and $500 comprehensive and collision deductibles. Read the detailed methodology for more information.

Get advice from an experienced insurance professional. Our experts will help you navigate your insurance questions with clarity and confidence.

Browse all FAQs